Following the introduction of margin transactions, Kei Hashimoto of the margin loan department at Japan Securities Finance provides an update and user guide of the Japanese stock trading method

Image: Kei Hashimoto

We introduced ‘margin transactions’, a unique Japanese stock trading method, in 2023. Following this, interest in the Japanese stock market has further increased, and as a result, there has been a growing interest in this trading method from outside Japan, which had been primarily utilised by domestic institutional and individual investors. Consequently, there has been an increase in the number of new participants in margin transactions and recipients of margin transaction information.

In general, to short shares, it is a global standard method to borrow these shares from securities companies who procure stocks from the stock lending market. However, market participants can use another unique method called margin transactions in Japan. The advantage of margin transactions is anyone can freely short the majority of more than 4,300 listed issues without complicated prior contracts, negotiations or paperwork with lenders.

Margin transactions account for approximately 15 per cent of the total trading value on the Tokyo Stock Exchange. Around 60-70 per cent of trading by individual investors involves margin transactions. Essentially, it has a large presence on the stock market in Japan.

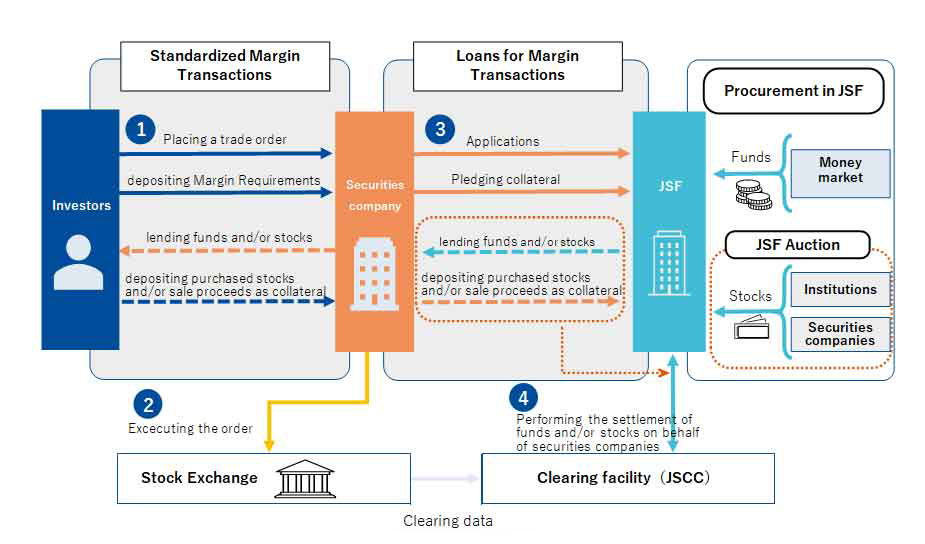

Margin transactions is the most utilised tool in Japan for investors to enter stock investments by short selling specific stocks or using short selling for hedging purposes of their existing stock holdings. Short selling is normally required to have shares procured in advance in countries with short selling regulations, including Japan. However, in standardised margin transactions (SMTs) in Japan, Japan Securities Finance (JSF) operates loans for margin transactions (LMTs) — an efficient stock procurement scheme.

Understanding the mechanics

A SMT is where an investor provides a certain amount of deposit (generally 30 per cent) to a securities company as collateral according to their own market forecast.

The investor then trades shares by borrowing the funds to buy the shares or the shares for sale from the securities company. These transactions are an effective investment tool which enables individual investors, who do not have direct access to the stock lending market, to improve capital efficiency and engage in stock investments by short selling specific stocks, just like professional investors. They are also widely recognised as a means of hedging risk of cash transaction position.

For instance, if a firm believes that the price of a certain stock will fall in the future, it can use a SMT to profit from this expectation. By using a SMT, the firm could borrow and sell those shares from a securities company only by placing a standardised margin selling order. It could then repurchase the shares when the price drops within the repayment period (up to six months in a SMT) and give them back to the securities company. The firm would then receive the difference in the selling price and the repurchase price. Moreover, as mentioned earlier, market participants can also avoid losses through hedge selling using SMT for hedging purposes (in other words, when one thinks the price of the shares held will drop) in addition to margin acquisition purposes.

Loans for margin transactions

Only securities finance companies licensed by the Prime Minister are provided to offer LMTs. JSF is the only such securities finance company in Japan. In principle, LMT participants are securities companies which are general trading participants of stock exchanges in Japan. Securities companies which have received trading orders for a SMT from their customers can procure the funds and shares necessary for settlement of the trade order by providing a certain level of collateral to JSF.

How does JSF procure the funds and shares necessary for LMT? With regard to funding, JSF can borrow the funds necessary from financial markets due to our high credit rating (S&P 'A' rating).

However, when it comes to stocks, they cannot be procured as easily as funds. Herein lies a major characteristic of LMT. In fact, JSF procures shares necessary from securities companies and institutional investors through an auction process (JSF Auction). While this auction is a means for JSF to procure stocks, it is also a highly attractive platform for stock utilisation in the Japanese stock lending market. JSF Auction is held every business day, on the day following the trade date, and the cost determined in the JSF Auction is called the ‘premium charge rate’.

An even more interesting point of this system is that this premium charge rate is applied to the entire SMT. Margin sellers pay a uniform premium charge according to the margin selling balance. On the other hand, auction participants and margin buyers can receive these premium charges according to the number of shares they successfully bid for and the margin buying balance.

From a data analysis perspective, the premium charge rate is an indicator which expresses the supply and demand of the Japanese stock lending market. If the premium charge rises sharply, it has the effect of encouraging margin sellers to clear their accounts and margin buyers to newly enter the market. Naturally, for the premium charge rate to occur, it is necessary for JSF's position to be short, so LMT is one of the major factors.

In general, the balance between margin buying and margin selling reaches an equilibrium through self-adjustment mechanism of the premium charge rate as mentioned earlier. Nevertheless, if the outlook for procurement through the auction process is unclear due to special factors such as sudden price fluctuations, corporate actions, and record date, JSF will issue a Notice for Precaution or restrict or suspend applications (prohibit new sales etc) in the use of stock loans according to the situation, thereby controlling the excessive increase in selling.

In this way, information such as the premium charge rate, LMT outstanding, and status of restrictive measures, greatly reflect the trends in the Japanese stock market and can be used to predict future stock price momentum. Inquiries from funds, primarily those considered to be quant-focused, have been increasing, and the level of interest has risen compared to before.

This data can be obtained from major financial vendors such as Bloomberg, Refinitiv, and Nasdaq Data Link, so we encourage market participants to consider acquiring them. Additionally, JSF published a theory on special index composition using these data, so those interested are to inquire with JSF.

Utilisation of margin selling

Again, firms can freely short 60 per cent of more than 4,300 listed issues without negotiating for stock procurement in SMT (that figure is more than 90 per cent in Prime Market). When any issues are eligible for margin selling and limited availability or high procurement costs on the stock lending market, how about considering shorting it using a SMT?

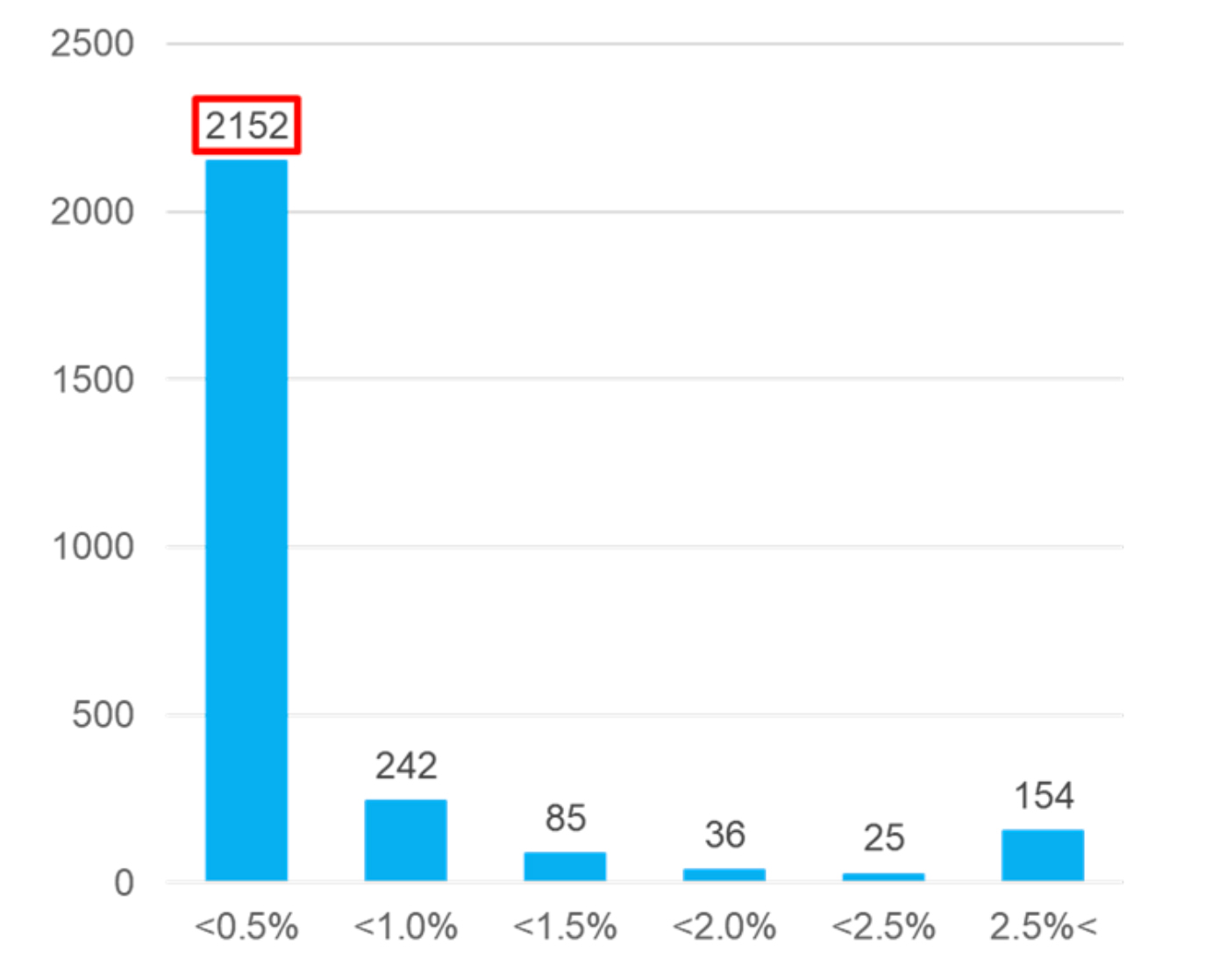

As previously described, the costs incurred in margin selling consist of the premium charge (there are also many issues which may not incur a premium charge) and the lending fee set by the securities company.

The premium charge is determined on the day after the trading date. Uncertainty remains because the procurement cost is finalised ex-post facto. However, looking at the historical data, there are many cases in which the costs involved in margin selling are lower than the cost of borrowing on the stock lending market. In particular, it is possible to find many issues which are comparatively less expensive if using margin selling among those which are difficult to borrow with high market rates.

One of the reasons for that is, so far, participation in the SMT market by professional investors has been limited (although, as mentioned at the beginning, the number of new participants is increasing recently) and most users tend to be individual investors in Japan. The preferences of professional investors and individual investors are often divided. Now, firms might be able to short Japanese stocks at a reasonable price with SMT without paying high fees on the stock lending market. As explained above, analysing historical data could reveal a lot of potential.

Conclusion

The mechanism of SMT is complicated. Nevertheless, it is a very interesting system unique to Japan which enables firms to short a wide range of issues. Firms can also start these transactions at any time by opening a margin trading account with a Japanese securities company, including its overseas branches or subsidiaries.

Furthermore, analysing this data might help firms to invest in Japanese stocks from a new and unprecedented perspective. Why not take this opportunity to once again focus on the stock market?

NO FEE, NO RISK 100% ON RETURNSIf you invest in only one securities finance news source this

year, make sure it is your free subscription to Securities Finance Times

Image: Kei Hashimoto

Image: Kei Hashimoto