The European cleared triparty repo market: a €500 billion digital bet

06 February 2024

Cyril Louchtchay de Fleurian, a consultant on repo markets and SFTs, examines a roadmap for growth and efficiency gains in European repo markets, including a case for the repositioning of GC Pooling and €GCplus solutions

Image: stock.adobe/ j-mel

Image: stock.adobe/ j-mel

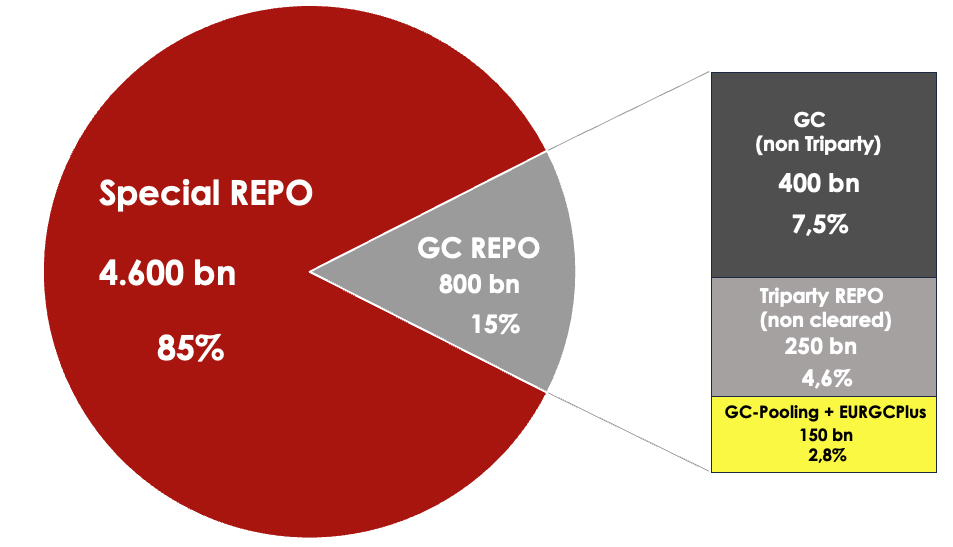

In the European repo market, securities financing operates through two primary channels. The first, special repo, facilitates the financing of a specific security against cash. This segment constitutes about 85 per cent of overall single-counted market volumes, totalling €4,600 billion according to data from the European Repo and Collateral Council dated June 2023.

Outstanding amounts in this category have grown in recent years, largely as a result of the impact of quantitative easing. This monetary policy has increased the value of the underlying securities, particularly sovereign securities. To maximise the value derived from these securities, transactions are conducted on an individual ISIN basis. Participants in this market have two options: they can either opt for clearing through a central counterparty or engage in direct face-to-face transactions.

The second avenue is the General Collateral (GC) market. This market segment facilitates the financing of a limited number of homogeneous securities, typically fewer than 10, in a single transaction, constituting approximately seven to eight per cent of the total market volumes, equivalent to €400 billion. Additionally, it accommodates the financing of a larger block of securities, occasionally comprising several hundred lines, grouped within a basket and specified by eligibility criteria. This larger block represents about seven to eight per cent of the overall volumes, totalling around €400 billion according to the ERCC survey cited above.

In the latter case, the large number of underlying lines has led some custodians to offer an outsourced collateral management service, a triparty repo service, encompassing activities including valuation, margin calls and substitution. Similar to the "specific" repo market, the triparty repo market offers the flexibility to trade repo on either a cleared or uncleared basis, with the uncleared segment representing roughly €250 billion. The baskets are both bilateral and specific to each pair of counterparties wishing to transact together.

Regarding the other sub-segment, clearing mechanisms have led the cleared triparty repo service to rely on standardised baskets designed to concentrate liquidity. Among the main baskets, one is "ECB eligible", reflecting monetary policy requirements, and the other is "compatible with LCR criteria", aligned with Basel Committee criteria for the Liquidity Coverage Ratio (LCR). This cleared triparty repo market is represented by two separate offers that are quasi-similar — EuroGCplus (€GCplus) and GCPooling — marketed by private market infrastructures LCH SA and Euroclear in the case of €GCplus, and Eurex Clearing and Clearstream for GC Pooling. To enhance liquidity, these GC products are accessible exclusively through electronic execution platforms. In one case, this is Brokertec and MTS (along with TP Repo to a lesser extent), while in the other it is the Eurex Repo trading platform.

Fig 1: European repo market

Single-counted outstanding €5,400 millions (doubled-counted €10,800 millions ERCC June 2023)

The value proposition offered by these cleared triparty repo platforms is unique, as their purpose is to serve as a key component of the interbank market, directly linked to monetary policy and European regulations. We are referring here to the secondary market for central bank liquidity and the market for high-quality liquid assets (HQLA) used to manage the LCR buffer. This explains the historical support from public authorities for the liquidity of these offerings, with the Banque de France supporting €GCplus and the German monetary authorities, namely Finanzagentur/KfW, supporting GC Pooling.

Despite this quasi-institutional support, the modest volumes in these two offers raises questions about their respective attractiveness — for European participants seeking financing and for the circulation of the underlying collateral, as well as for the appeal of the European financial space on the international stage. The combined outstanding amount has reached approximately €150 billion, representing about 2.8 per cent of the global repo market, with €GCplus accounting for €10 billion and GC Pooling accounting for €140 billion.

The limited appetite from banks might, on initial scrutiny, indicate specific technical shortcomings in the product offers. More worrisome is that this scenario could also signify a questionable strategic positioning. Given the present operational landscape for the European infrastructure ecosystem, friction may appear insurmountable for participants. Indeed, in the context of a supposedly vast and deep European market, the presence of two competing solutions with the same liquidity objective, based on the same product, raises questions.

In essence, it is possible that these offers, as they are currently presented in the market, could generate friction and, in doing so, impact both liquidity and the transmission of monetary policy. In essence, there is a possibility that these solutions, in their current form, fall short of fully realising the market's potential.

To some extent, the US market can provide comparative insights: it totals US$7.1 trillion in outstanding, with a cleared GC repo market (equivalent to the European GC Pooling and €GCplus perimeter) valued at US$650 billion (approximately nine per cent of the total outstanding), with US$400 billion in agency MBS baskets and US$250 billion in US treasuries, according to figures from the New York Federal Reserve. The management of the US platform is centralised by the Fixed Income Clearing Corporation (FICC), a subsidiary of the Depository Trust and Clearing Corporation. Therefore, in the segment we are considering, the European market is proportionally six to seven times narrower than the American one. Although these two markets are not perfectly comparable, the magnitude of the difference between them is noteworthy.

In evaluating the potential offered by the European market, we will aggregate some market figures and derive a potential volume projection. Let us assume that the cleared triparty repo market relies on the following elements:

• The total single-counted size of the European repo market (€5.4 trillion).

• The size of the interbank cleared bilateral repo market (approximately €1.7 trillion).

• The size of the ECB balance sheet, which is approximately €9 trillion — including around €2.2 trillion for main refinancing operations (MRO) and longer-term refinancing operations (LTRO); and €5 trillion for the Asset Purchase Programme (APP) and Public Sector Purchase Programmes (PSPP).

• Liquidity surplus of €4.2 trillion.

• The total of €3.6 trillion held at the ECB deposit facility on an overnight basis.

• The number of banks in the Eurozone, which is close to 2,400 on a consolidated basis.

• Estimated needs in HQLA securities.

• The number of ISINs included in ECB eligible baskets and LCR-compliant baskets.

Our analysis assumes that the European cleared triparty repo market could potentially reach €500 billion — representing approximately eight to 10 per cent of the overall European repo market — deviating over three standard deviations from the observed market average (i.e. €150 billion). More than the absolute figure, it is once again the magnitude of the deviation from the market reality that is noteworthy.

The narratives for these two platforms diverge significantly, despite having a very similar business model. GC Pooling emerged in the early 2000s and, until 2007, volumes remained at 10-20 billion. It then increased significantly during the 2008-9 crisis, reaching 180 billion in 2014. Despite liquidity injections and interest rate cuts, the freeze in the interbank market and the persistent context of latent European crisis clearly drove volumes upwards. However, from 2014 to 2017, as unconventional monetary policy became the standard practice, interbank tensions eased, GC Pooling volumes plummeted from 180 billion to 40 billion, remaining at these levels until 2021. The rate hikes in 2022 once again boosted the outstanding volumes, which currently total 140 billion.

Several factors contributed to these volumes. From 2007 to 2014, GC Pooling served as a key "anti-crisis" instrument, facilitating the anonymous acquisition of liquidity without counterparty risk as banks faced the clearing house.

From 2015 to 2021, the stable yet modest residual base of 40 billion was primarily fuelled by the demand for HQLA and arbitrage, rather than liquidity requirements. However, despite less accommodative monetary policy and significant collateral needs, the platform appears to encounter a glass ceiling. In essence, the German model has demonstrated an inability to realise its full potential over several years. This limitation stems from a model that is excessively "siloed" and domestic, lacking interoperability and no longer aligning with the demands of a neutral and integrated European ecosystem.

As for €GCplus, the storyline is less vibrant precisely because the platform never truly took off. Launched too late, in 2011, under the name Collateral Basket With Pledge (CBWP) — amid the European chaos of the 2010-12 crisis — the intention was commendable, but the offer did not meet the technical expectations of the banks. It was rebranded as EuroGCplus (€GCplus) in 2014 and relaunched belatedly in 2014-2016, even as the market was flooded with liquidity.

Despite being supported by the Banque de France, which saw this as a way to compete with the liquidity of the German silo, volumes have remained marginal so far. Regarding its strategic positioning, weaknesses are similar to those for GC Pooling, with some additional unresolved functional biases making efficiency, and therefore onboarding of new clients, problematic.

The intention here is not to delve into the technical details of the two offers individually, but rather to highlight more generic issues. As the offers stem from the cross-collaboration of a triparty agent and a clearing house, weaknesses sometimes arise from one, sometimes from the other, and sometimes from an unfortunate synergy of both.

The first point of attention concerns the narrow scope of eligible securities and its daily update. The number of eligible securities varies by twofold between these offers and, at most, covers only 60 to 65 per cent of ECB-eligible securities as a whole.

A second relates to the structure of the baskets of securities; allocation criteria are complex, burdened by unclear concentration criteria.

The third concerns issues with the reuse of securities. These are not systematically reusable in non-cleared triparty repo tools, neither towards the central bank nor towards clearing houses.

A fourth point of concern relates to operational netting, which is not always feasible with individually-allocated sovereign securities in bilateral repo transactions.

A fifth constraint relates to the opening hours of the service — deemed too restrictive — especially for transactions settled on a same-day basis.

While this list is not exhaustive, it does emphasise the range, and often the complexity, of the issues encountered. These challenges disrupt the value chain, serving as obstacles to volume growth. Nonetheless, it is important to note that these issues are essentially technical or commercial in nature and can be addressed, provided that promoters (typically triparty agents and clearing houses) and distributors (typically trading platforms) prioritise and allocate the necessary resources. These factors partially explain the lack of momentum in €GCplus and the subdued dynamics of GC Pooling. However, the crux of the matter likely lies elsewhere.

The analysis reveals that the duality in the market of two very similar offerings ultimately undermines the original value proposition, deviating from the intended purpose. The foundation of this proposition lies in a uniform and neutral access point, referring to shared interests and objectives that benefit the entire financial community in the region. It represents the infrastructure, resources and conditions considered advantageous for the proper functioning and development of monetary policy.

Progress is still needed in this area. Specifically, the original value proposition is based on the neutral and agnostic nature of the central bank's secondary liquidity, the fluidity of collateral movements, and transparency. This nature transcends national and private interests to achieve a unique, balanced solution beneficial to all members of the Eurosystem.

In the first contribution to this three-part article, I have particularly examined synergies in clearing and triparty repo. The second part, in the next issue of SFT, will look more closely at the ecosystem supporting use of general collateral baskets in Europe and potential designs for repositioning GC Pooling and €GCplus.

Outstanding amounts in this category have grown in recent years, largely as a result of the impact of quantitative easing. This monetary policy has increased the value of the underlying securities, particularly sovereign securities. To maximise the value derived from these securities, transactions are conducted on an individual ISIN basis. Participants in this market have two options: they can either opt for clearing through a central counterparty or engage in direct face-to-face transactions.

The second avenue is the General Collateral (GC) market. This market segment facilitates the financing of a limited number of homogeneous securities, typically fewer than 10, in a single transaction, constituting approximately seven to eight per cent of the total market volumes, equivalent to €400 billion. Additionally, it accommodates the financing of a larger block of securities, occasionally comprising several hundred lines, grouped within a basket and specified by eligibility criteria. This larger block represents about seven to eight per cent of the overall volumes, totalling around €400 billion according to the ERCC survey cited above.

In the latter case, the large number of underlying lines has led some custodians to offer an outsourced collateral management service, a triparty repo service, encompassing activities including valuation, margin calls and substitution. Similar to the "specific" repo market, the triparty repo market offers the flexibility to trade repo on either a cleared or uncleared basis, with the uncleared segment representing roughly €250 billion. The baskets are both bilateral and specific to each pair of counterparties wishing to transact together.

Regarding the other sub-segment, clearing mechanisms have led the cleared triparty repo service to rely on standardised baskets designed to concentrate liquidity. Among the main baskets, one is "ECB eligible", reflecting monetary policy requirements, and the other is "compatible with LCR criteria", aligned with Basel Committee criteria for the Liquidity Coverage Ratio (LCR). This cleared triparty repo market is represented by two separate offers that are quasi-similar — EuroGCplus (€GCplus) and GCPooling — marketed by private market infrastructures LCH SA and Euroclear in the case of €GCplus, and Eurex Clearing and Clearstream for GC Pooling. To enhance liquidity, these GC products are accessible exclusively through electronic execution platforms. In one case, this is Brokertec and MTS (along with TP Repo to a lesser extent), while in the other it is the Eurex Repo trading platform.

Fig 1: European repo market

Single-counted outstanding €5,400 millions (doubled-counted €10,800 millions ERCC June 2023)

The value proposition offered by these cleared triparty repo platforms is unique, as their purpose is to serve as a key component of the interbank market, directly linked to monetary policy and European regulations. We are referring here to the secondary market for central bank liquidity and the market for high-quality liquid assets (HQLA) used to manage the LCR buffer. This explains the historical support from public authorities for the liquidity of these offerings, with the Banque de France supporting €GCplus and the German monetary authorities, namely Finanzagentur/KfW, supporting GC Pooling.

Despite this quasi-institutional support, the modest volumes in these two offers raises questions about their respective attractiveness — for European participants seeking financing and for the circulation of the underlying collateral, as well as for the appeal of the European financial space on the international stage. The combined outstanding amount has reached approximately €150 billion, representing about 2.8 per cent of the global repo market, with €GCplus accounting for €10 billion and GC Pooling accounting for €140 billion.

The limited appetite from banks might, on initial scrutiny, indicate specific technical shortcomings in the product offers. More worrisome is that this scenario could also signify a questionable strategic positioning. Given the present operational landscape for the European infrastructure ecosystem, friction may appear insurmountable for participants. Indeed, in the context of a supposedly vast and deep European market, the presence of two competing solutions with the same liquidity objective, based on the same product, raises questions.

In essence, it is possible that these offers, as they are currently presented in the market, could generate friction and, in doing so, impact both liquidity and the transmission of monetary policy. In essence, there is a possibility that these solutions, in their current form, fall short of fully realising the market's potential.

To some extent, the US market can provide comparative insights: it totals US$7.1 trillion in outstanding, with a cleared GC repo market (equivalent to the European GC Pooling and €GCplus perimeter) valued at US$650 billion (approximately nine per cent of the total outstanding), with US$400 billion in agency MBS baskets and US$250 billion in US treasuries, according to figures from the New York Federal Reserve. The management of the US platform is centralised by the Fixed Income Clearing Corporation (FICC), a subsidiary of the Depository Trust and Clearing Corporation. Therefore, in the segment we are considering, the European market is proportionally six to seven times narrower than the American one. Although these two markets are not perfectly comparable, the magnitude of the difference between them is noteworthy.

In evaluating the potential offered by the European market, we will aggregate some market figures and derive a potential volume projection. Let us assume that the cleared triparty repo market relies on the following elements:

• The total single-counted size of the European repo market (€5.4 trillion).

• The size of the interbank cleared bilateral repo market (approximately €1.7 trillion).

• The size of the ECB balance sheet, which is approximately €9 trillion — including around €2.2 trillion for main refinancing operations (MRO) and longer-term refinancing operations (LTRO); and €5 trillion for the Asset Purchase Programme (APP) and Public Sector Purchase Programmes (PSPP).

• Liquidity surplus of €4.2 trillion.

• The total of €3.6 trillion held at the ECB deposit facility on an overnight basis.

• The number of banks in the Eurozone, which is close to 2,400 on a consolidated basis.

• Estimated needs in HQLA securities.

• The number of ISINs included in ECB eligible baskets and LCR-compliant baskets.

Our analysis assumes that the European cleared triparty repo market could potentially reach €500 billion — representing approximately eight to 10 per cent of the overall European repo market — deviating over three standard deviations from the observed market average (i.e. €150 billion). More than the absolute figure, it is once again the magnitude of the deviation from the market reality that is noteworthy.

The narratives for these two platforms diverge significantly, despite having a very similar business model. GC Pooling emerged in the early 2000s and, until 2007, volumes remained at 10-20 billion. It then increased significantly during the 2008-9 crisis, reaching 180 billion in 2014. Despite liquidity injections and interest rate cuts, the freeze in the interbank market and the persistent context of latent European crisis clearly drove volumes upwards. However, from 2014 to 2017, as unconventional monetary policy became the standard practice, interbank tensions eased, GC Pooling volumes plummeted from 180 billion to 40 billion, remaining at these levels until 2021. The rate hikes in 2022 once again boosted the outstanding volumes, which currently total 140 billion.

Several factors contributed to these volumes. From 2007 to 2014, GC Pooling served as a key "anti-crisis" instrument, facilitating the anonymous acquisition of liquidity without counterparty risk as banks faced the clearing house.

From 2015 to 2021, the stable yet modest residual base of 40 billion was primarily fuelled by the demand for HQLA and arbitrage, rather than liquidity requirements. However, despite less accommodative monetary policy and significant collateral needs, the platform appears to encounter a glass ceiling. In essence, the German model has demonstrated an inability to realise its full potential over several years. This limitation stems from a model that is excessively "siloed" and domestic, lacking interoperability and no longer aligning with the demands of a neutral and integrated European ecosystem.

As for €GCplus, the storyline is less vibrant precisely because the platform never truly took off. Launched too late, in 2011, under the name Collateral Basket With Pledge (CBWP) — amid the European chaos of the 2010-12 crisis — the intention was commendable, but the offer did not meet the technical expectations of the banks. It was rebranded as EuroGCplus (€GCplus) in 2014 and relaunched belatedly in 2014-2016, even as the market was flooded with liquidity.

Despite being supported by the Banque de France, which saw this as a way to compete with the liquidity of the German silo, volumes have remained marginal so far. Regarding its strategic positioning, weaknesses are similar to those for GC Pooling, with some additional unresolved functional biases making efficiency, and therefore onboarding of new clients, problematic.

The intention here is not to delve into the technical details of the two offers individually, but rather to highlight more generic issues. As the offers stem from the cross-collaboration of a triparty agent and a clearing house, weaknesses sometimes arise from one, sometimes from the other, and sometimes from an unfortunate synergy of both.

The first point of attention concerns the narrow scope of eligible securities and its daily update. The number of eligible securities varies by twofold between these offers and, at most, covers only 60 to 65 per cent of ECB-eligible securities as a whole.

A second relates to the structure of the baskets of securities; allocation criteria are complex, burdened by unclear concentration criteria.

The third concerns issues with the reuse of securities. These are not systematically reusable in non-cleared triparty repo tools, neither towards the central bank nor towards clearing houses.

A fourth point of concern relates to operational netting, which is not always feasible with individually-allocated sovereign securities in bilateral repo transactions.

A fifth constraint relates to the opening hours of the service — deemed too restrictive — especially for transactions settled on a same-day basis.

While this list is not exhaustive, it does emphasise the range, and often the complexity, of the issues encountered. These challenges disrupt the value chain, serving as obstacles to volume growth. Nonetheless, it is important to note that these issues are essentially technical or commercial in nature and can be addressed, provided that promoters (typically triparty agents and clearing houses) and distributors (typically trading platforms) prioritise and allocate the necessary resources. These factors partially explain the lack of momentum in €GCplus and the subdued dynamics of GC Pooling. However, the crux of the matter likely lies elsewhere.

The analysis reveals that the duality in the market of two very similar offerings ultimately undermines the original value proposition, deviating from the intended purpose. The foundation of this proposition lies in a uniform and neutral access point, referring to shared interests and objectives that benefit the entire financial community in the region. It represents the infrastructure, resources and conditions considered advantageous for the proper functioning and development of monetary policy.

Progress is still needed in this area. Specifically, the original value proposition is based on the neutral and agnostic nature of the central bank's secondary liquidity, the fluidity of collateral movements, and transparency. This nature transcends national and private interests to achieve a unique, balanced solution beneficial to all members of the Eurosystem.

In the first contribution to this three-part article, I have particularly examined synergies in clearing and triparty repo. The second part, in the next issue of SFT, will look more closely at the ecosystem supporting use of general collateral baskets in Europe and potential designs for repositioning GC Pooling and €GCplus.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times