Collateral management: Biscuit or cake?

19 November 2020

Understanding the history of a favourite snack in the UK and the former Yugoslav republics can help us think about how to design collateral management departments and systems

Image: stock.adobe.com/Lovrencg

Image: stock.adobe.com/Lovrencg

Walk into a supermarket anywhere in the Yugoslav republics and you are likely to be confronted in the biscuit section by a large selection of a very British snack, the Jaffa Cake, a snack invented by Scottish biscuit manufacturer McVitie and Price in 1927. Though biscuit sized, sold next to biscuits and eaten as an alternative to biscuits to accompany hot beverages, Jaffa Cakes have some very non-biscuit-like qualities. A Jaffa Cake consists of three layers: a sponge base, an orange jelly layer and a covering of dark chocolate.

But what does this have to with collateral management?

Jaffa Cakes in their 93 years of existence have seen an explosion in variety. There are multiple manufacturers and flavours and they are even available in milk instead of dark chocolate. Yet, all the varieties are clearly identifiable as the same sweet snack. Likewise, so is collateral management. The process of giving and receiving collateral in the form of cash or securities has also grown in a very wide variety of forms. Some of the more recent forms are driven by financial innovation but many of the others resulting from tougher regulation in the light of the great financial crisis.

The other parallel is the biscuit or cake dilemma. Jaffa Cakes have been involved in legal disputes in both the UK and Ireland relating to whether they are cakes or biscuits. For collateral management the question is whether it is a revenue generating front office activity or operational activity where the focus should be efficiency and control.

In the UK, Her Majesty’s Customs and Revenue (HMRC) has long agonised about the classification of Jaffa Cakes. To quote its website: “Customs and Excise had accepted since the start of VAT that Jaffa cakes were zero-rated as cakes, but always had misgivings about whether this was correct.” In 1991, it decided to take action and imposed value added tax on Jaffa Cakes. McVities, the inventor and primary manufacturer appealed. The nation held its breath and sipped its tea as highly-paid lawyers debated the question. To demonstrate the fundamentally cake-like properties of Jaffa Cakes, McVities baked a giant cake-sized Jaffa Cake. In the end the court decided on the essentials. If a Jaffa Cake was left exposed to the air for a long time, what would happen? Biscuits that are left exposed grow soggy, while cakes, if left exposed, grow dry and hard. Science demonstrated the exposed Jaffa became dry and hard, like a cake. The judgement was made and consumption continued, untaxed. In Ireland a similar case was solved even more scientifically based on the moisture content of Jaffa cakes compared to the average moisture content of biscuits and other cakes.

The equivalent judgement in the front or back office dilemma for collateral management is, firstly, to understand why the question matters, secondly, to identify the criteria for making the decision. For Jaffa Cakes the question of cake or biscuit mattered for tax reasons. In collateral management the question of where it belongs in a firm’s organisational structure matters for the following reasons:

• The choice of collateral provided has a direct impact on the profit-and-loss and risk positions of a firm

• Whether it is in the front office or operations has important implications for segregation of duty

• It influences the design of systems used for collateral management and the data they need contain and process

Before looking at the answer to that question it is worth considering the sheer range of types of collateral management that have emerged, often performed by different teams or systems within the same organisations. For much of their history collateral management systems focused on margin management for over-the-counter derivatives. Separate collateral processes existed in products such as futures, contracts for difference (CFDs) and securities lending, where the margin process was essentially integrated into the trade lifecycle. Forms of collateral management evolved where collateral management was placed with a third party rather than bilaterally exchanged, where the agent arranging trades received/managed collateral, where trades were cleared and both parties faced a central counterparty (CCP) and where cleared trades were executed via a clearing broker (see Figure 1).

Figure 1

The problem with so many variations was how to identify the key elements that made collateral management. Only by identifying the essential characteristics (sponge, jelly and chocolate in the case of a Jaffa Cake) is it possible to design systems and operating models that allow a holistic approach to collateral management as opposed to progressively more complex systems and departments.

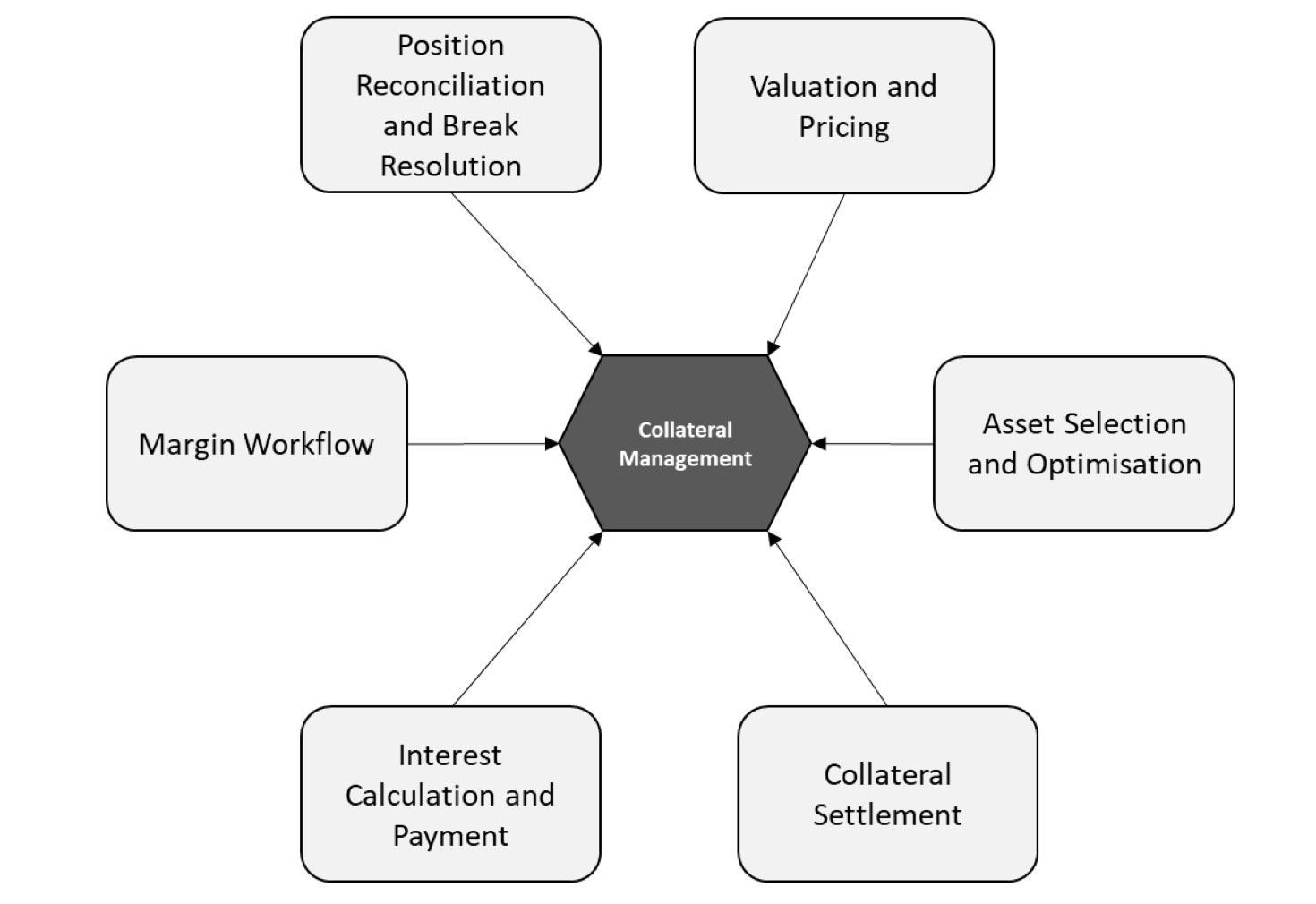

Looking across all the variations (see Figure 2) does reveal a small set of common themes, though in some cases the activity is performed outside the core collateral management system or department.

Figure 2

Position reconciliation and break resolution: reconciling positions and resolving breaks is a process well served in different flavours of collateral management by different processes and systems. Securities lending has contract compare processes, OTC derivatives has a portfolio reconciliation while other flavours rely on a centralised golden source of the truth. A centralised collateral management department/system therefore needs to be able to integrate with reconciliation tools that are outside their direct control.

Valuation and pricing: valuations of trades and pricing of collateral to feed into exposure calculations are also functions carried out most effectively in other systems, so the central team/system needs to interact with incoming price and valuations feeds, rather than generate themselves.

Collateral settlements: the management of settlements is another area where other systems and teams are specialised in carrying out these activities and the key need is to have a clearly defined and implemented interface between collateral management teams/systems and settlements/payments. Though integrating collateral related settlements into a collateral management team or system can significantly reduce communication errors between both systems and people.

Margin workflow: This is the area that needs to have most flexibility because depending on the type of collateral management it is likely there are different participants involved, different degrees of straight-through-processing (STP) and different parties driving the overall process. For instance, if a CCP is involved it is likely the CCP’s view of the trade would be treated as the golden source, valuations and margin calls will be driven by the CCP rather than the parties that originally entered it into the trade.

Interest calculation and payment: The use of cash as a form of collateral, particularly as variation margin and the processing of other cash flows from collateral (such as coupons on bonds) mean there is a general requirement to calculate interest and other cash flows. As with some of the other processes, depending on the asset class and type of trading, it is likely that the collateral management department/system will need to be able to perform calculations but also integrate to other systems and teams where calculations are more tightly integrated into the lifecycle of products.

The final area to consider that is common to almost all forms of collateral management is Asset Selection. It is consideration of asset selection that answers collateral management’s “biscuit or cake” question, “is collateral management a front or back office activity?”

The optimal choice of assets to deliver as collateral (or substitute/recall) is influenced by multiple factors including:

• The acceptable set of collateral as specified in a credit support annex or other relevant legal document that specifies eligible collateral

• The opportunity cost of using collateral including potential returns/costs of using securities in securities lending/repo or cash

• The impact on measures such as the leverage ratio, liquidity coverage ratio and risk weighted assets

• Settlement costs of transferring collateral or positioning collateral in the right location

• The impact of client relations of recalling or substituting collateral

Making the correct decisions fundamentally needs a consideration of both risk and profitability i.e. front-office tasks. Fortunately, algorithms can be configured to have the appropriate objectives and constraints and can do most of the thinking, subject to a degree of human supervision and fine tuning. Leaving exception management and most of the client interaction to more operationally focused staff.

Overall, the combination of skills, activities and data required for effective collateral management make it an activity that is aligned to both trading and operations. In addition to a wide range of functionality and interfaces, a good collateral management system therefore requires a sophisticated permission-based model to control access to both functionality and data to avoid segregation of duty issues and the risk of fraudulent activities.

Depending on the skillset, size and location of the team it is also necessary to have sufficient flexibility built into core workflows to either add in additional four eye checks or allow maximum STP. The properly designed system and department is therefore far superior to a Jaffa Cake but does not provide such a good accompaniment to tea or coffee.

But what does this have to with collateral management?

Jaffa Cakes in their 93 years of existence have seen an explosion in variety. There are multiple manufacturers and flavours and they are even available in milk instead of dark chocolate. Yet, all the varieties are clearly identifiable as the same sweet snack. Likewise, so is collateral management. The process of giving and receiving collateral in the form of cash or securities has also grown in a very wide variety of forms. Some of the more recent forms are driven by financial innovation but many of the others resulting from tougher regulation in the light of the great financial crisis.

The other parallel is the biscuit or cake dilemma. Jaffa Cakes have been involved in legal disputes in both the UK and Ireland relating to whether they are cakes or biscuits. For collateral management the question is whether it is a revenue generating front office activity or operational activity where the focus should be efficiency and control.

In the UK, Her Majesty’s Customs and Revenue (HMRC) has long agonised about the classification of Jaffa Cakes. To quote its website: “Customs and Excise had accepted since the start of VAT that Jaffa cakes were zero-rated as cakes, but always had misgivings about whether this was correct.” In 1991, it decided to take action and imposed value added tax on Jaffa Cakes. McVities, the inventor and primary manufacturer appealed. The nation held its breath and sipped its tea as highly-paid lawyers debated the question. To demonstrate the fundamentally cake-like properties of Jaffa Cakes, McVities baked a giant cake-sized Jaffa Cake. In the end the court decided on the essentials. If a Jaffa Cake was left exposed to the air for a long time, what would happen? Biscuits that are left exposed grow soggy, while cakes, if left exposed, grow dry and hard. Science demonstrated the exposed Jaffa became dry and hard, like a cake. The judgement was made and consumption continued, untaxed. In Ireland a similar case was solved even more scientifically based on the moisture content of Jaffa cakes compared to the average moisture content of biscuits and other cakes.

The equivalent judgement in the front or back office dilemma for collateral management is, firstly, to understand why the question matters, secondly, to identify the criteria for making the decision. For Jaffa Cakes the question of cake or biscuit mattered for tax reasons. In collateral management the question of where it belongs in a firm’s organisational structure matters for the following reasons:

• The choice of collateral provided has a direct impact on the profit-and-loss and risk positions of a firm

• Whether it is in the front office or operations has important implications for segregation of duty

• It influences the design of systems used for collateral management and the data they need contain and process

Before looking at the answer to that question it is worth considering the sheer range of types of collateral management that have emerged, often performed by different teams or systems within the same organisations. For much of their history collateral management systems focused on margin management for over-the-counter derivatives. Separate collateral processes existed in products such as futures, contracts for difference (CFDs) and securities lending, where the margin process was essentially integrated into the trade lifecycle. Forms of collateral management evolved where collateral management was placed with a third party rather than bilaterally exchanged, where the agent arranging trades received/managed collateral, where trades were cleared and both parties faced a central counterparty (CCP) and where cleared trades were executed via a clearing broker (see Figure 1).

Figure 1

The problem with so many variations was how to identify the key elements that made collateral management. Only by identifying the essential characteristics (sponge, jelly and chocolate in the case of a Jaffa Cake) is it possible to design systems and operating models that allow a holistic approach to collateral management as opposed to progressively more complex systems and departments.

Looking across all the variations (see Figure 2) does reveal a small set of common themes, though in some cases the activity is performed outside the core collateral management system or department.

Figure 2

Position reconciliation and break resolution: reconciling positions and resolving breaks is a process well served in different flavours of collateral management by different processes and systems. Securities lending has contract compare processes, OTC derivatives has a portfolio reconciliation while other flavours rely on a centralised golden source of the truth. A centralised collateral management department/system therefore needs to be able to integrate with reconciliation tools that are outside their direct control.

Valuation and pricing: valuations of trades and pricing of collateral to feed into exposure calculations are also functions carried out most effectively in other systems, so the central team/system needs to interact with incoming price and valuations feeds, rather than generate themselves.

Collateral settlements: the management of settlements is another area where other systems and teams are specialised in carrying out these activities and the key need is to have a clearly defined and implemented interface between collateral management teams/systems and settlements/payments. Though integrating collateral related settlements into a collateral management team or system can significantly reduce communication errors between both systems and people.

Margin workflow: This is the area that needs to have most flexibility because depending on the type of collateral management it is likely there are different participants involved, different degrees of straight-through-processing (STP) and different parties driving the overall process. For instance, if a CCP is involved it is likely the CCP’s view of the trade would be treated as the golden source, valuations and margin calls will be driven by the CCP rather than the parties that originally entered it into the trade.

Interest calculation and payment: The use of cash as a form of collateral, particularly as variation margin and the processing of other cash flows from collateral (such as coupons on bonds) mean there is a general requirement to calculate interest and other cash flows. As with some of the other processes, depending on the asset class and type of trading, it is likely that the collateral management department/system will need to be able to perform calculations but also integrate to other systems and teams where calculations are more tightly integrated into the lifecycle of products.

The final area to consider that is common to almost all forms of collateral management is Asset Selection. It is consideration of asset selection that answers collateral management’s “biscuit or cake” question, “is collateral management a front or back office activity?”

The optimal choice of assets to deliver as collateral (or substitute/recall) is influenced by multiple factors including:

• The acceptable set of collateral as specified in a credit support annex or other relevant legal document that specifies eligible collateral

• The opportunity cost of using collateral including potential returns/costs of using securities in securities lending/repo or cash

• The impact on measures such as the leverage ratio, liquidity coverage ratio and risk weighted assets

• Settlement costs of transferring collateral or positioning collateral in the right location

• The impact of client relations of recalling or substituting collateral

Making the correct decisions fundamentally needs a consideration of both risk and profitability i.e. front-office tasks. Fortunately, algorithms can be configured to have the appropriate objectives and constraints and can do most of the thinking, subject to a degree of human supervision and fine tuning. Leaving exception management and most of the client interaction to more operationally focused staff.

Overall, the combination of skills, activities and data required for effective collateral management make it an activity that is aligned to both trading and operations. In addition to a wide range of functionality and interfaces, a good collateral management system therefore requires a sophisticated permission-based model to control access to both functionality and data to avoid segregation of duty issues and the risk of fraudulent activities.

Depending on the skillset, size and location of the team it is also necessary to have sufficient flexibility built into core workflows to either add in additional four eye checks or allow maximum STP. The properly designed system and department is therefore far superior to a Jaffa Cake but does not provide such a good accompaniment to tea or coffee.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times