Taking stress out of mid-life events

26 April 2022

The optimal way to manage mid-life trade maintenance is to transact on a centralised electronic trading platform that standardises traditional and complex trade structures and streamlines manual, risk-prone event workflows, says Sal Giglio, chief operating officer, GLMX

Image: Sal Giglio

Image: Sal Giglio

On 16 March 2022, the Federal Reserve’s Open Market Committee (FOMC) raised the federal funds rate by 25 basis points. This was the first time the Fed moved the rate since reducing it by 100 basis points on 15 March 2020 at the onset of the COVID-19 pandemic. With inflation at its highest level in 40 years, the FOMC indicated that this will be the first of many more rate increases to come. The Bank of England‘s Monetary Policy Committee (MPC) also raised the Bank Rate by 25 basis points on the same day.

Although short term interest rate movements create opportunities for securities finance trading desks to generate significant revenue, they also create a lot of work in the form of trade maintenance. Market events lead to an increase in activity and can generate sizeable, hard-to-manage increases in operational activity. Changes in monetary policy drive mid-life events like rate adjustments to variable-rate trades. Unfortunately, trade maintenance is often manual and, therefore, both error-prone and time-consuming.

In many respects, the manual process supporting a securities financing transaction (SFT) relates to the old adage about a duck sitting on a pond: “On the surface everything looks calm, but beneath the water its feet are churning a mile a minute”. Once a trade occurs, a flurry of activity ensues to ensure the transacted securities and cash make it to the agreed destination in the agreed timeframe. Traders, salespeople, assistants and mid-office personnel communicate trade details with each other, and with their trade counterparts, through a variety of media including chats, emails, third-party electronic confirmations, phone calls and, believe it or not, via fax. Beneath the surface, or post trade, settlement risk is created due to the traditional market practice which requires both parties to manually enter trade details into their own position management systems.

Given the risk and attendant high cost of manual trade entry errors, affirming trade details prior to settlement is essential. This often entails a time-consuming two-step process. The front office of the sell-side firm delivers a written communication of the trade details to its buy-side counterparty and then, prior to settlement, the back offices of each firm verify, often by phone, chat or email, that the matched trade details were entered correctly into each firm’s system.

This is an important, but highly inefficient and inadequately addressed, aspect of the financing market. International Capital Markets Association’s (ICMA) European Repo and Collateral Council (ERCC) Operations Group publishes a standardised template for trade matching and affirmation of repo transactions. According to the ICMA website, “affirmation in the repo market is the process of one party seeking urgent validation from the other of the key economic terms and settlement addresses of selected transactions, either immediately after execution or during the life of a transaction after any material change to that information”. The ICMA also indicates that “currently, affirmation is a manual process in which the operations group of one party telephones or e-mails the operations area of the other party, lists the key economic terms and settlement addresses of the selected transactions or any material changes and requests the other party to immediately agree or identify details on which they disagree.”

To add another level of operational complexity not seen in other markets, securities finance transactions have two settlement legs, the start-leg (start date) and the close-leg (maturity), and for many trade structures mid-life trade maintenance is required. Mid-life trade events can take many forms and these events are mainly driven by either the need to maintain flexibility around the pledged collateral — such as early termination, repricing, substitution, and resizing — or to manage the risk parameters of the trade such as rerating and cleaning up accrued financing interest.

Intricate trade structures include variable-rate open and term maturity, puttable/callable, extendable and evergreen. These trade structures exist to provide flexibility around collateral, to lock in certainty of liquidity, to reduce leveraged capital exposure, and to avoid fixed rate interest rate exposure while reducing settlement risk. As with new trades, these material mid-life changes need to be affirmed by both parties and can create operational bottlenecks on high volume days.

The future is now

The industry has tried to address the operational risks associated with manual trade inputs but the results have been costly and incomplete. Intraday third-party electronic matching services require double keying for one or both parties and still result in trade mismatches. End-of-day post-trade comparison services require both the sell-side and the buy-side institutions to be clients of the same service and to manually deliver a daily file or build direct connectivity. However, trades that require same-day settlement — which represent a large percentage of transactions in the US — present a significant challenge to such services in that the ‘matching’ is asynchronous. Said plainly, a communication error in any single link of the complex communication chain can go unnoticed until well after the fact of the trade.

The ideal way to address these manual, inefficient and risk-prone workflows is to transact on a centralised electronic trading platform that standardises both traditional and complex trade structures and streamlines mid-life event workflows, while also providing pre and post-trade connectivity to trade capture systems, central counterparties, triparty providers, prime brokers and custodians. At their core, electronic trading platforms are synchronised communication systems which mitigate the operational risks associated with manual processes and eliminate the need for an inefficient affirmation process, since trade details are digitally affirmed by both parties at the point of the trade and straight-through processing (STP) eliminates trade input risk. This comprehensive technology is precisely what GLMX provides to its clients today.

Since its launch, GLMX has supported mid-life trade maintenance through its native user interface (UI) and full STP connectivity. Through an interactive blotter accessed through the trading UI, users can action mid-life events, including variable rate trade structures with open and term maturities, trades that have optionality such as puttables/callables, evergreens and extendables, and collateral management needs through substitutions and resizing of trades. These actions are bilateral and automatically flow into each counterparty’s system, reducing workflow friction and mitigating operational risk.

The GLMX experience

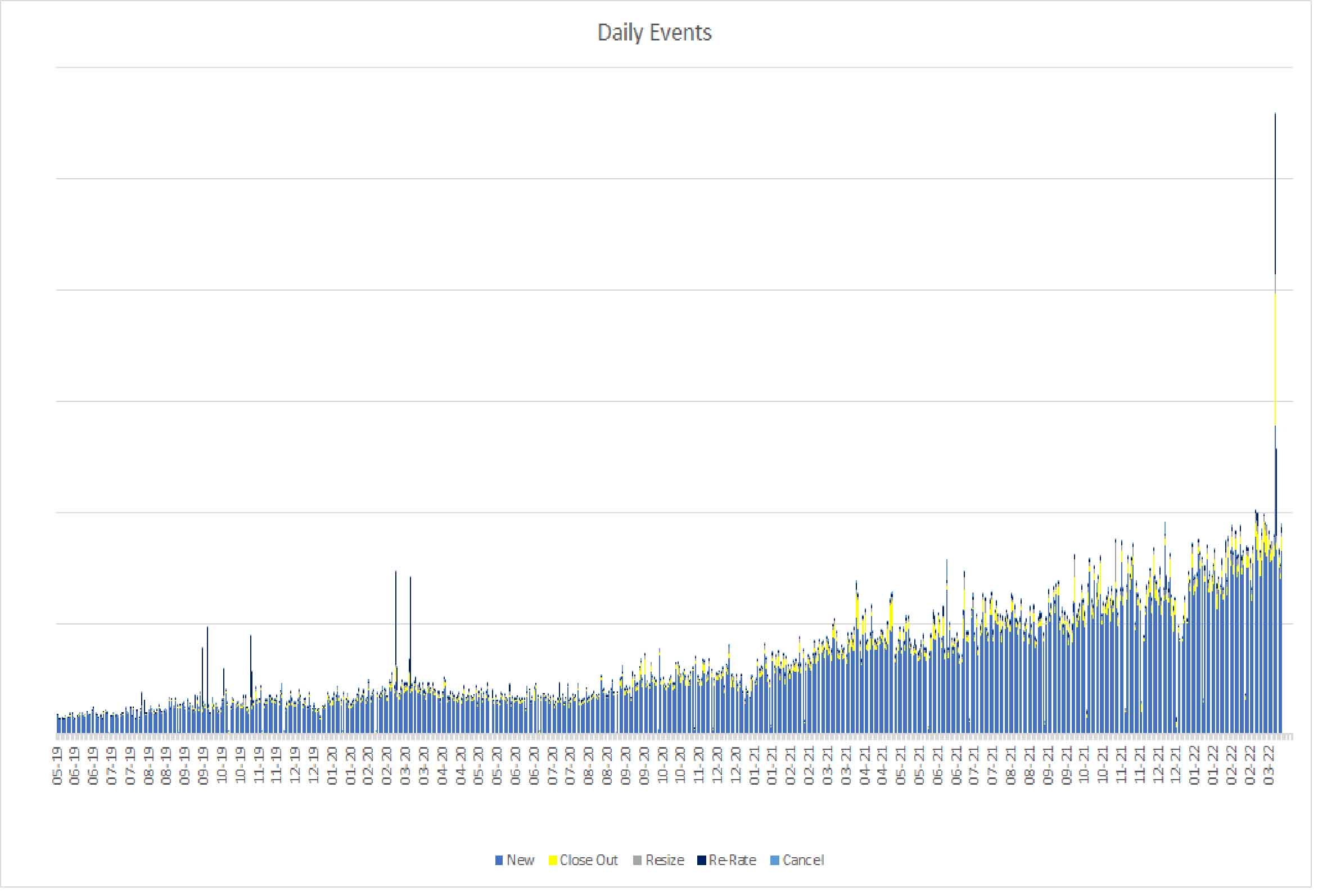

On 17 March, as a result of the previous day’s change in monetary policy by the Fed and the Bank of England, GLMX experienced a 3.5-times increase in trade events on its platform compared with the previous 20-day average. Trade events included new trades, close outs, resizes, rerates and cancels. Not surprisingly, re-rating of variable-rate trades accounted for the majority of the increase in activity. Since user trade-capture technology is varied, GLMX accommodates re-rating in several ways: first, by tracking the new rate and calculating accrued interest based on that new rate; second, by utilising GLMX resizing functionality in which the existing trade is closed and a new trade is automatically created with a new rate; and, third, by initiating mass closeouts, followed immediately by opening new positions — all via a single upload.

GLMX provides automation to support high volume days (see 17 March 2022 on the chart below) to help clients efficiently manage their increased workflow and minimise risk of mistakes.

Post 17 March, both buy and sell-side clients praised the smooth and seamless experience rerating variable rate trades using GLMX technology. In fact, one client compared the experience of rerating their corporate book on GLMX versus rerating their smaller emerging markets (EM) book, which has not yet completed onboarding to the GLMX platform. They were effusive about how the automated GLMX process was measured in minutes, while the manual off-platform process was measured in hours.

While the full power of GLMX technology shines on days such as 17 March, the daily impact of digitally streamlining the complete securities finance trading workflow — pre-trade, trade and post-trade – is similarly powerful. Combining GLMX’s advanced trading functionality with STP, new trades and mid-life events are handled more efficiently and GLMX, as the single source of mutually agreed trade accuracy from the moment of execution, drives further efficiencies and provides a convenient gateway for managing regulatory requirements such as best execution, Securities Financing Transactions Regulation (SFTR) and the Central Securities Depositories Regulation (CSDR).

In sum, digitised SFT negotiation and execution, such as that uniquely offered by GLMX, provide an enormous leap in the quest to minimise operational friction, transaction, fail and regulatory costs.

Although short term interest rate movements create opportunities for securities finance trading desks to generate significant revenue, they also create a lot of work in the form of trade maintenance. Market events lead to an increase in activity and can generate sizeable, hard-to-manage increases in operational activity. Changes in monetary policy drive mid-life events like rate adjustments to variable-rate trades. Unfortunately, trade maintenance is often manual and, therefore, both error-prone and time-consuming.

In many respects, the manual process supporting a securities financing transaction (SFT) relates to the old adage about a duck sitting on a pond: “On the surface everything looks calm, but beneath the water its feet are churning a mile a minute”. Once a trade occurs, a flurry of activity ensues to ensure the transacted securities and cash make it to the agreed destination in the agreed timeframe. Traders, salespeople, assistants and mid-office personnel communicate trade details with each other, and with their trade counterparts, through a variety of media including chats, emails, third-party electronic confirmations, phone calls and, believe it or not, via fax. Beneath the surface, or post trade, settlement risk is created due to the traditional market practice which requires both parties to manually enter trade details into their own position management systems.

Given the risk and attendant high cost of manual trade entry errors, affirming trade details prior to settlement is essential. This often entails a time-consuming two-step process. The front office of the sell-side firm delivers a written communication of the trade details to its buy-side counterparty and then, prior to settlement, the back offices of each firm verify, often by phone, chat or email, that the matched trade details were entered correctly into each firm’s system.

This is an important, but highly inefficient and inadequately addressed, aspect of the financing market. International Capital Markets Association’s (ICMA) European Repo and Collateral Council (ERCC) Operations Group publishes a standardised template for trade matching and affirmation of repo transactions. According to the ICMA website, “affirmation in the repo market is the process of one party seeking urgent validation from the other of the key economic terms and settlement addresses of selected transactions, either immediately after execution or during the life of a transaction after any material change to that information”. The ICMA also indicates that “currently, affirmation is a manual process in which the operations group of one party telephones or e-mails the operations area of the other party, lists the key economic terms and settlement addresses of the selected transactions or any material changes and requests the other party to immediately agree or identify details on which they disagree.”

To add another level of operational complexity not seen in other markets, securities finance transactions have two settlement legs, the start-leg (start date) and the close-leg (maturity), and for many trade structures mid-life trade maintenance is required. Mid-life trade events can take many forms and these events are mainly driven by either the need to maintain flexibility around the pledged collateral — such as early termination, repricing, substitution, and resizing — or to manage the risk parameters of the trade such as rerating and cleaning up accrued financing interest.

Intricate trade structures include variable-rate open and term maturity, puttable/callable, extendable and evergreen. These trade structures exist to provide flexibility around collateral, to lock in certainty of liquidity, to reduce leveraged capital exposure, and to avoid fixed rate interest rate exposure while reducing settlement risk. As with new trades, these material mid-life changes need to be affirmed by both parties and can create operational bottlenecks on high volume days.

The future is now

The industry has tried to address the operational risks associated with manual trade inputs but the results have been costly and incomplete. Intraday third-party electronic matching services require double keying for one or both parties and still result in trade mismatches. End-of-day post-trade comparison services require both the sell-side and the buy-side institutions to be clients of the same service and to manually deliver a daily file or build direct connectivity. However, trades that require same-day settlement — which represent a large percentage of transactions in the US — present a significant challenge to such services in that the ‘matching’ is asynchronous. Said plainly, a communication error in any single link of the complex communication chain can go unnoticed until well after the fact of the trade.

The ideal way to address these manual, inefficient and risk-prone workflows is to transact on a centralised electronic trading platform that standardises both traditional and complex trade structures and streamlines mid-life event workflows, while also providing pre and post-trade connectivity to trade capture systems, central counterparties, triparty providers, prime brokers and custodians. At their core, electronic trading platforms are synchronised communication systems which mitigate the operational risks associated with manual processes and eliminate the need for an inefficient affirmation process, since trade details are digitally affirmed by both parties at the point of the trade and straight-through processing (STP) eliminates trade input risk. This comprehensive technology is precisely what GLMX provides to its clients today.

Since its launch, GLMX has supported mid-life trade maintenance through its native user interface (UI) and full STP connectivity. Through an interactive blotter accessed through the trading UI, users can action mid-life events, including variable rate trade structures with open and term maturities, trades that have optionality such as puttables/callables, evergreens and extendables, and collateral management needs through substitutions and resizing of trades. These actions are bilateral and automatically flow into each counterparty’s system, reducing workflow friction and mitigating operational risk.

The GLMX experience

On 17 March, as a result of the previous day’s change in monetary policy by the Fed and the Bank of England, GLMX experienced a 3.5-times increase in trade events on its platform compared with the previous 20-day average. Trade events included new trades, close outs, resizes, rerates and cancels. Not surprisingly, re-rating of variable-rate trades accounted for the majority of the increase in activity. Since user trade-capture technology is varied, GLMX accommodates re-rating in several ways: first, by tracking the new rate and calculating accrued interest based on that new rate; second, by utilising GLMX resizing functionality in which the existing trade is closed and a new trade is automatically created with a new rate; and, third, by initiating mass closeouts, followed immediately by opening new positions — all via a single upload.

GLMX provides automation to support high volume days (see 17 March 2022 on the chart below) to help clients efficiently manage their increased workflow and minimise risk of mistakes.

Post 17 March, both buy and sell-side clients praised the smooth and seamless experience rerating variable rate trades using GLMX technology. In fact, one client compared the experience of rerating their corporate book on GLMX versus rerating their smaller emerging markets (EM) book, which has not yet completed onboarding to the GLMX platform. They were effusive about how the automated GLMX process was measured in minutes, while the manual off-platform process was measured in hours.

While the full power of GLMX technology shines on days such as 17 March, the daily impact of digitally streamlining the complete securities finance trading workflow — pre-trade, trade and post-trade – is similarly powerful. Combining GLMX’s advanced trading functionality with STP, new trades and mid-life events are handled more efficiently and GLMX, as the single source of mutually agreed trade accuracy from the moment of execution, drives further efficiencies and provides a convenient gateway for managing regulatory requirements such as best execution, Securities Financing Transactions Regulation (SFTR) and the Central Securities Depositories Regulation (CSDR).

In sum, digitised SFT negotiation and execution, such as that uniquely offered by GLMX, provide an enormous leap in the quest to minimise operational friction, transaction, fail and regulatory costs.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times