The entry of pension funds into Eurex’s cleared repo markets creates a win-win situation

07 May 2022

As the temporary central clearing exemption granted by the European Commission expires, Frank Odendall, Eurex’s head of securities financing, product and business development, finds that pension funds are voluntarily looking to CCP clearing for both mandatory and non-mandatory products, including repo

Image: stock.adobe.com/jozefmicic

Image: stock.adobe.com/jozefmicic

The next few years will mark a new era in the relationships between pension scheme arrangements (PSAs) and clearing houses, driven in most part by the forthcoming expiry of the temporary exemption from the obligation to centrally clear over-the-counter (OTC) derivatives transactions. In granting an exemption to PSAs, the European Commission recognised a range of structural issues that needed to be resolved before they could be brought into scope. As those issues come closer to resolution, numerous PSAs are pre-empting the expiry and voluntarily adopting clearing for both mandatory and non-mandatory products and asset classes, including repo.

Repo plays an integral role in the financial markets by linking participants who lend and borrow short-term against securities pledged as collateral, providing a key source of funding and a substitute for unsecured deposits. The special and general collateral segments enhance the utility of the repo market by providing a means of financing securities portfolios and a mechanism for sourcing valuable collateral, which is of critical importance given the level of quantitative easing.

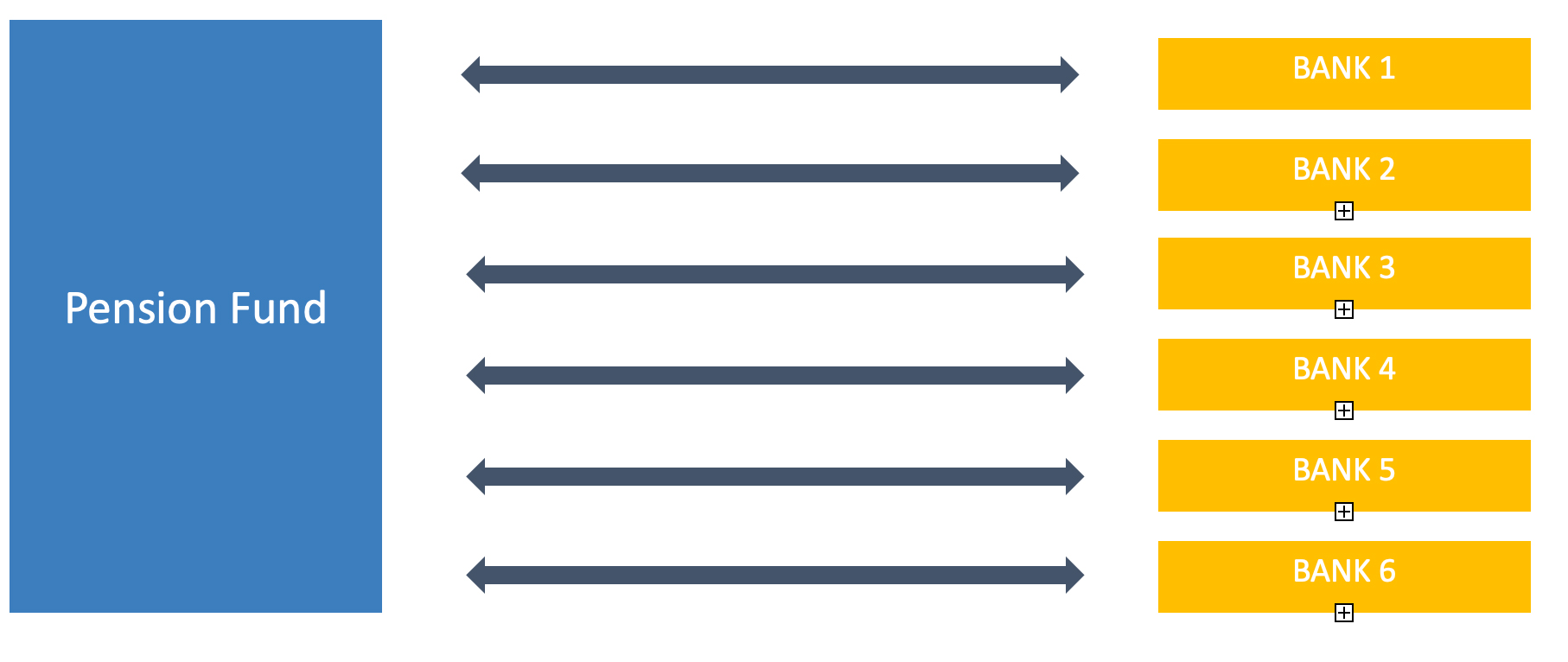

In the bilateral market, PSAs have to maintain multiple bilateral relationships with a range of sell-side institutions, each with their own customised contractual commitments, and this is costly on several levels (see figure 1). It is time consuming and labour intensive to both establish and maintain these relationships, and repo transactions are often still negotiated by phone or fax. These types of relationships also make price discovery and regulatory reporting burdensome and costly, adding to this inefficiency.

Figure 1

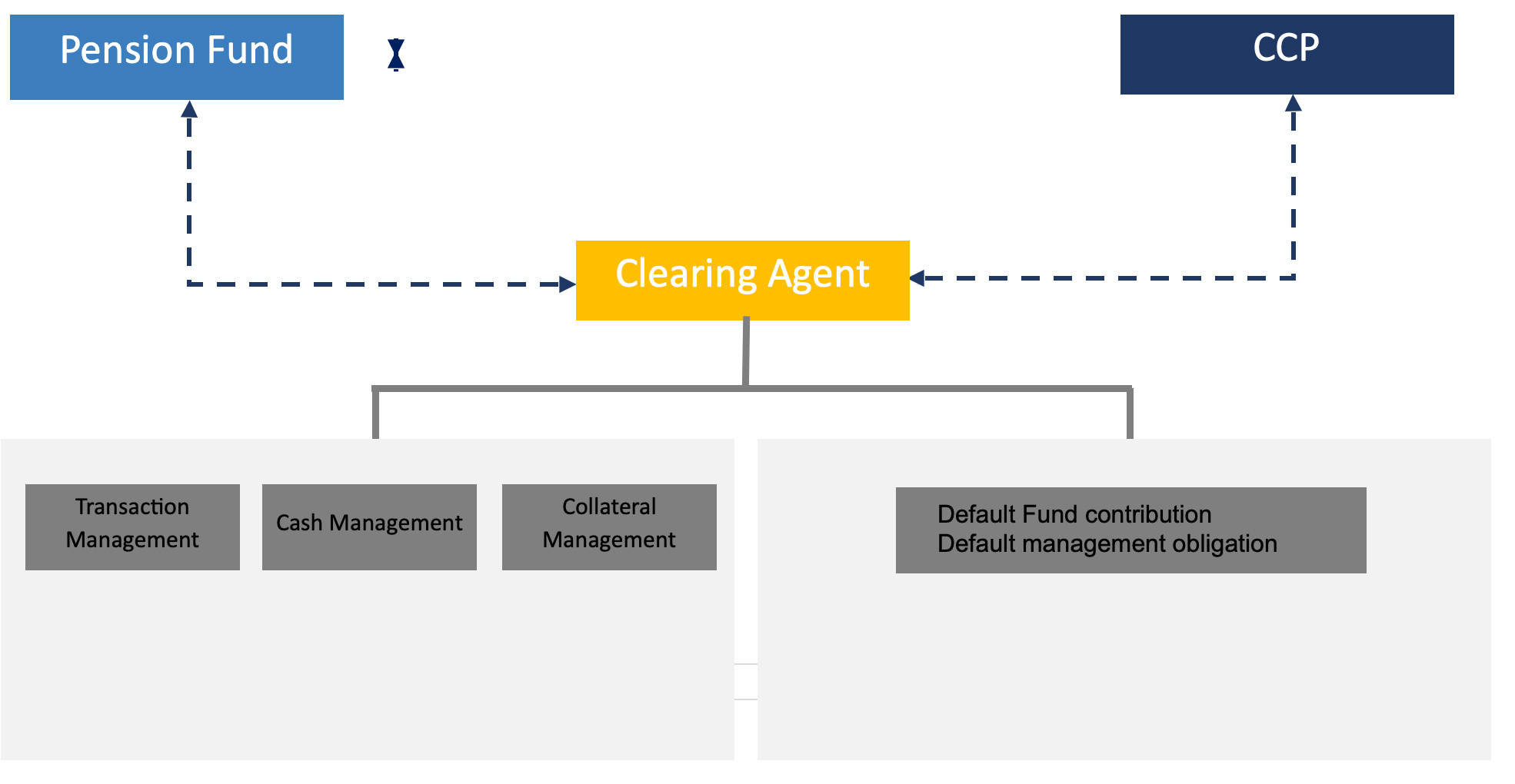

Centrally cleared repo markets are a natural evolution of the bilateral markets, bringing new efficiencies for market participants with additional benefits for market stability. Eurex’s ISA Direct clearing model for repo is the industry-leading solution for PSAs to enter the cleared repo market, whereby the PSA faces the clearing house directly but is supported by a clearing agent that covers the default fund contributions and default management obligations (see figure 2).

Figure 2

Cleared repos that are electronically executed via a multilateral trading, facility such as Eurex Repo, offer a range of advantages for PSA participants. Most importantly, PSAs can re-invest or raise cash for Variation Margin (VM) for Eurex-cleared OTC interest rate swaps (IRS) more efficiently and securely by accessing the Eurex Repo GC Pooling cash-driven repo market. In this paper, we explore some of the many use cases in more detail.

PSA perspective

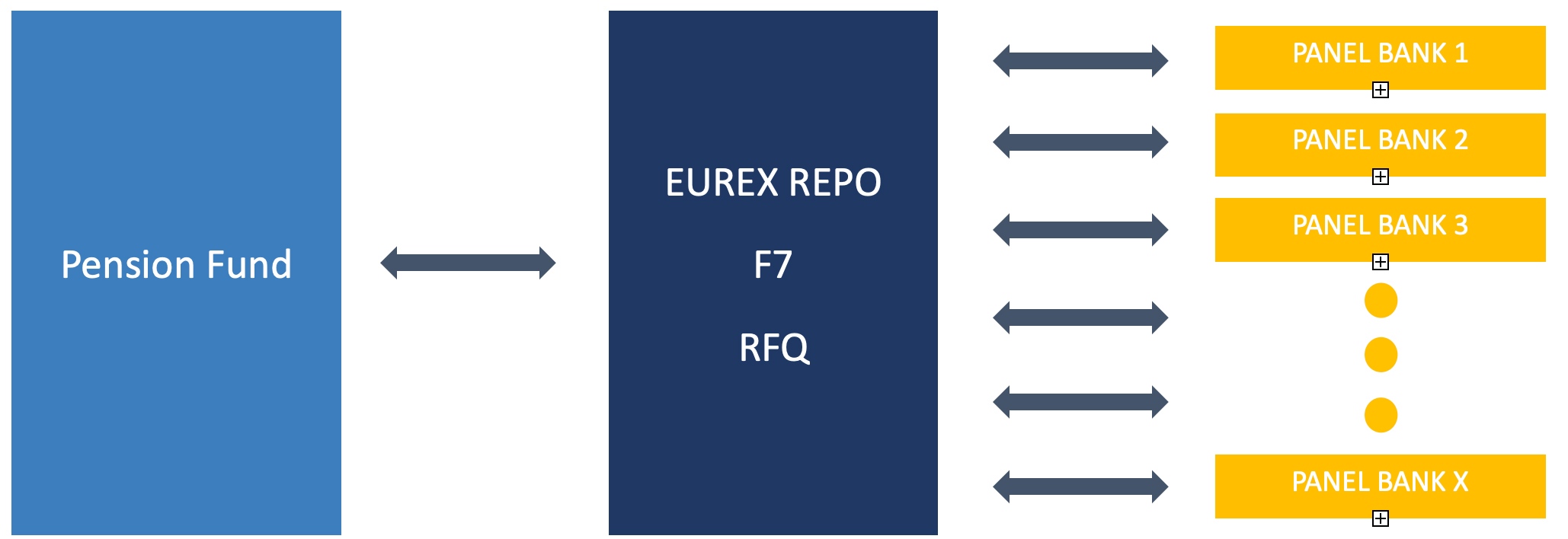

PSAs are now live with Eurex’s cleared repo offering, and actively place excess cash in the overnight and term cleared repo markets. Each PSA has established a panel of dealer banks and utilises the Eurex Repo F7 request for quote (RFQ) functionality (see Figure 3). The PSAs trade on the most competitive quote available from the panel banks. Based on feedback received, the rates are understood to be better than those achievable through money market funds and also usually better than the bilateral markets.

Figure 3

The key benefits for PSAs are summarised below:

• deep, pan-European liquidity pool means improved price discovery

• over 150 participants are registered with Eurex Repo, including commercial and central banks, and government financing agencies

• secure raising and placing of cash against more than 13,000 domestic and international securities

• centrally-cleared markets with proven liquidity in times of stress

• reduced indirect constraints from punitive bank capital requirements

• streamlined and efficient electronic processes

• standardisation of legal documentation

• greater control and flexibility to counterparty risk management across cleared and bilateral markets

• optimal management of margin funding requirements for cleared and uncleared derivatives

• Dealer perspective

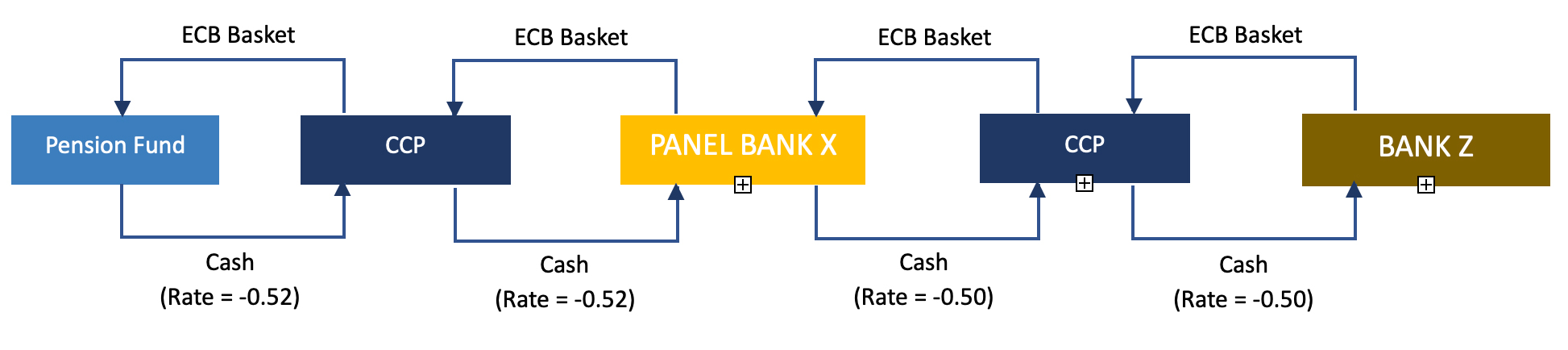

Cleared repo markets in Europe have historically been the domain of banks that trade repo anonymously via the order book and the trade is subsequently novated to the clearing house. Feedback indicates that where a panel bank’s response to the RFQ is successful, the bank borrows cash at a better rate (1-2bps cheaper) than achieved in the interbank market through the order book.

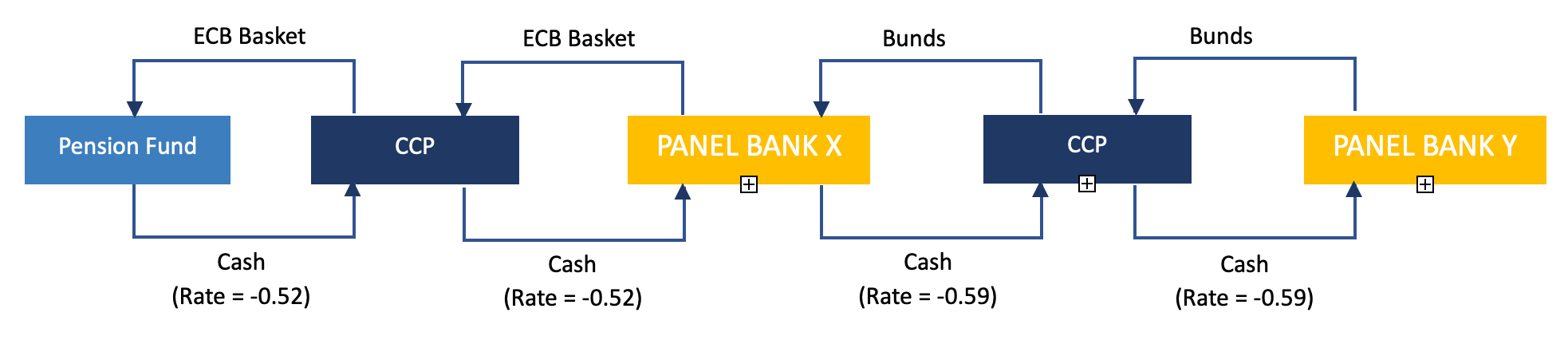

If the panel bank raises funding more cheaply than it can raise in the interbank market, it can immediately lend the cash in the interbank market and earn a spread as illustrated in Figure 4. Alternatively, the panel bank can use the cheap funding it raises from the Pension Fund to finance its ‘specials’ trading as illustrated in Figure 5.

Figure 4

Figure 5

The core advantage for the dealer bank in either the spread trading or the specials trading use cases is the ability to trade in a capital and balance sheet efficient manner. First, low risk weights (2 per cent) are applied to trades facing CCPs. Second, in both use cases the two cash legs for Panel Bank X are offsetting (i.e. nettable). However, there are several criteria that must be achieved before balance sheet netting can be applied under the accounting standards and prudential regulation. Eurex and Clearstream’s integrated trading, clearing and settlement infrastructure is well-placed to help banks meet the stringent criteria under the standards, enabling them to achieve the maximum capital and balance sheet efficiencies available.

Summary

There are numerous benefits available to pension funds as they enter the clearing landscape, including enhanced liquidity, operational efficiencies, streamlined legal documentation and effective counterparty risk management.

The dealer bank community has also benefited substantially from the entry of pension funds into the clearing landscape. Aside from new trading opportunities, the entry of buy-side firms into the cleared environment enhances the ability to realise the valuable potential of multilateral netting and balance sheet netting not otherwise available in the bilateral environment.

The new era promises to deliver a win-win situation for all market participants.

Repo plays an integral role in the financial markets by linking participants who lend and borrow short-term against securities pledged as collateral, providing a key source of funding and a substitute for unsecured deposits. The special and general collateral segments enhance the utility of the repo market by providing a means of financing securities portfolios and a mechanism for sourcing valuable collateral, which is of critical importance given the level of quantitative easing.

In the bilateral market, PSAs have to maintain multiple bilateral relationships with a range of sell-side institutions, each with their own customised contractual commitments, and this is costly on several levels (see figure 1). It is time consuming and labour intensive to both establish and maintain these relationships, and repo transactions are often still negotiated by phone or fax. These types of relationships also make price discovery and regulatory reporting burdensome and costly, adding to this inefficiency.

Figure 1

Centrally cleared repo markets are a natural evolution of the bilateral markets, bringing new efficiencies for market participants with additional benefits for market stability. Eurex’s ISA Direct clearing model for repo is the industry-leading solution for PSAs to enter the cleared repo market, whereby the PSA faces the clearing house directly but is supported by a clearing agent that covers the default fund contributions and default management obligations (see figure 2).

Figure 2

Cleared repos that are electronically executed via a multilateral trading, facility such as Eurex Repo, offer a range of advantages for PSA participants. Most importantly, PSAs can re-invest or raise cash for Variation Margin (VM) for Eurex-cleared OTC interest rate swaps (IRS) more efficiently and securely by accessing the Eurex Repo GC Pooling cash-driven repo market. In this paper, we explore some of the many use cases in more detail.

PSA perspective

PSAs are now live with Eurex’s cleared repo offering, and actively place excess cash in the overnight and term cleared repo markets. Each PSA has established a panel of dealer banks and utilises the Eurex Repo F7 request for quote (RFQ) functionality (see Figure 3). The PSAs trade on the most competitive quote available from the panel banks. Based on feedback received, the rates are understood to be better than those achievable through money market funds and also usually better than the bilateral markets.

Figure 3

The key benefits for PSAs are summarised below:

• deep, pan-European liquidity pool means improved price discovery

• over 150 participants are registered with Eurex Repo, including commercial and central banks, and government financing agencies

• secure raising and placing of cash against more than 13,000 domestic and international securities

• centrally-cleared markets with proven liquidity in times of stress

• reduced indirect constraints from punitive bank capital requirements

• streamlined and efficient electronic processes

• standardisation of legal documentation

• greater control and flexibility to counterparty risk management across cleared and bilateral markets

• optimal management of margin funding requirements for cleared and uncleared derivatives

• Dealer perspective

Cleared repo markets in Europe have historically been the domain of banks that trade repo anonymously via the order book and the trade is subsequently novated to the clearing house. Feedback indicates that where a panel bank’s response to the RFQ is successful, the bank borrows cash at a better rate (1-2bps cheaper) than achieved in the interbank market through the order book.

If the panel bank raises funding more cheaply than it can raise in the interbank market, it can immediately lend the cash in the interbank market and earn a spread as illustrated in Figure 4. Alternatively, the panel bank can use the cheap funding it raises from the Pension Fund to finance its ‘specials’ trading as illustrated in Figure 5.

Figure 4

Figure 5

The core advantage for the dealer bank in either the spread trading or the specials trading use cases is the ability to trade in a capital and balance sheet efficient manner. First, low risk weights (2 per cent) are applied to trades facing CCPs. Second, in both use cases the two cash legs for Panel Bank X are offsetting (i.e. nettable). However, there are several criteria that must be achieved before balance sheet netting can be applied under the accounting standards and prudential regulation. Eurex and Clearstream’s integrated trading, clearing and settlement infrastructure is well-placed to help banks meet the stringent criteria under the standards, enabling them to achieve the maximum capital and balance sheet efficiencies available.

Summary

There are numerous benefits available to pension funds as they enter the clearing landscape, including enhanced liquidity, operational efficiencies, streamlined legal documentation and effective counterparty risk management.

The dealer bank community has also benefited substantially from the entry of pension funds into the clearing landscape. Aside from new trading opportunities, the entry of buy-side firms into the cleared environment enhances the ability to realise the valuable potential of multilateral netting and balance sheet netting not otherwise available in the bilateral environment.

The new era promises to deliver a win-win situation for all market participants.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times