The fairest of them all

19 May 2023

Best execution and fair allocation are inextricably bound in the business of securities lending. Mike Lambert, head of securities lending product, Securities Finance and Collateral Management at Broadridge, explores the challenges of algorithms and the fiduciary responsibilities of lending agents

Image: Mike Lambert

Image: Mike Lambert

When it comes to securities lending there is a perennial question — “Is it fair?”.

“Is what fair?”, I hear you ask.

Let’s talk about fair algorithms and just how fair the securities lending business really is. In the agency securities lending world, agents have many fiduciary responsibilities to their underlying clients, be they UCITS funds, family offices or retail clients. These responsibilities encompass many areas outside of the scope of this article, so for the benefit of clarity we will focus on just two of the responsibilities — best execution and fair allocation.

These two concepts are inextricably bound in the business of securities lending, so we cannot talk about one without addressing the other. Before discussing the main topic, it is important to define best execution and fair allocation.

Best execution

“‘Best execution’ means that, when firms execute client orders, they must take all reasonable steps to deliver the best possible result for their clients, taking into account a variety of factors, such as the price of the financial instrument, speed of execution of the order and cost. For retail clients, ‘best possible’ means the most favourable result in terms of the price of the instrument and the costs associated with the execution.”

The above is just one of many definitions of best execution from various European Securities and Markets Authority (ESMA) sources, but there are also legal opinions and a number of different perspectives from members of the International Securities Lending Association (ISLA) and the International Capital Market Association (ICMA).

Fair allocation

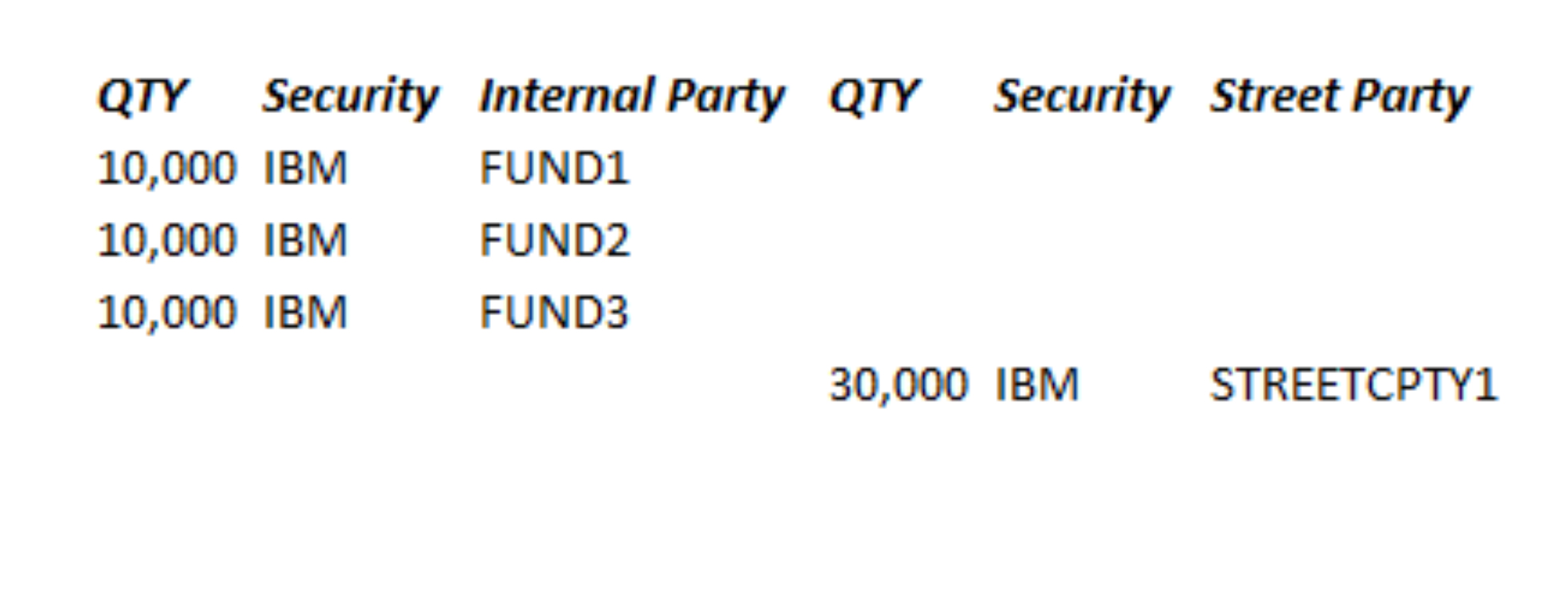

With an agency lending trade there are two parties, we have the “street” party, which is the borrower — this could be a prime broker, principal borrower or other sell-side party — and the “internal” party, which is the agent’s internal client — this could be a pension fund, UCITS or any buy-side entity. For example, a generic agency trade.

Figure 1

In the above example, there are three funds lending an aggregate quantity of 30,000 to “STREETCPTY1”.

Borrowers do not want to have piecemeal trades with small quantities, which is why agent lenders aggregate their availability so that they can complete the order in one hit.

The agent lender could have thousands of possible internal clients to select from to fill the trade. The question is — which internal clients should they select for the trade? This is the essence of fair allocation.

There is more than one way to skin the proverbial cat, as is the case with fair allocation. The models that are currently used within the industry can be broken down into variations of several models.

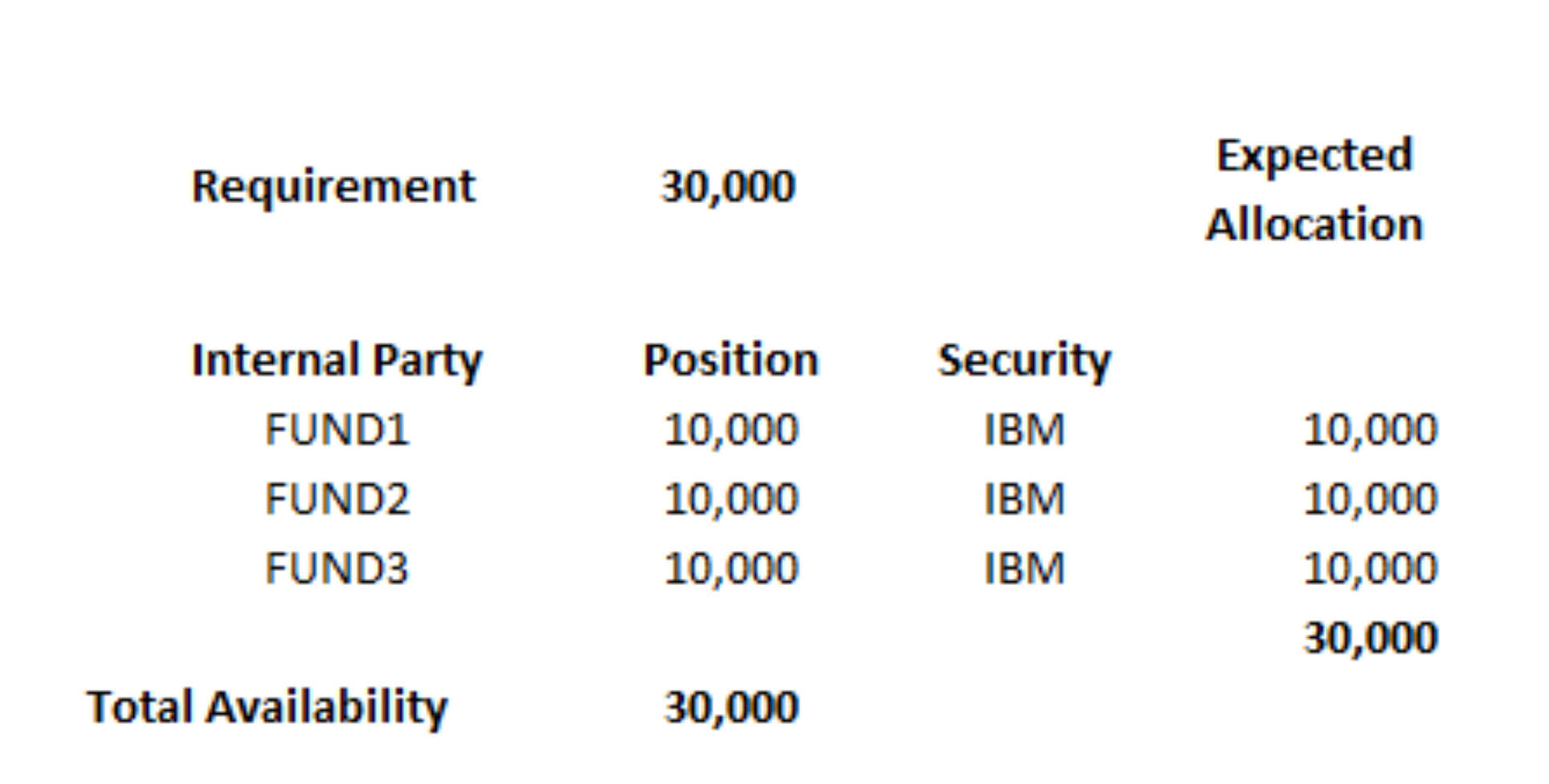

In the equal-allocation model, every internal party gets allocated an equal portion of the trade regardless of the size of parties holding. Although seemingly fair, the downside to this model is the sheer volume of internal allocations that it can generate. It is conceivable to have hundreds, if not thousands, of allocations for a single trade. This can prove expensive for the agent, as each allocation potentially has an associated settlement cost — which can be passed on to the internal client in the form of charges.

A further downside is that the more parties you have on a trade, the more likely it is that firms will have to do a daily reallocation, as the odds are higher, some of the parties that have lent out their shares will have sold them and will need to recall the shares to fulfil the sale. Those parties’ allocation will have to be replaced with shares from another party, otherwise the trade will have to be partially recalled. This issue is not limited to just this allocation model, it applies to any method that creates a large number of allocations.

For the equal-allocation model, the required quantity is equally split among clients with availability.

Figure 2

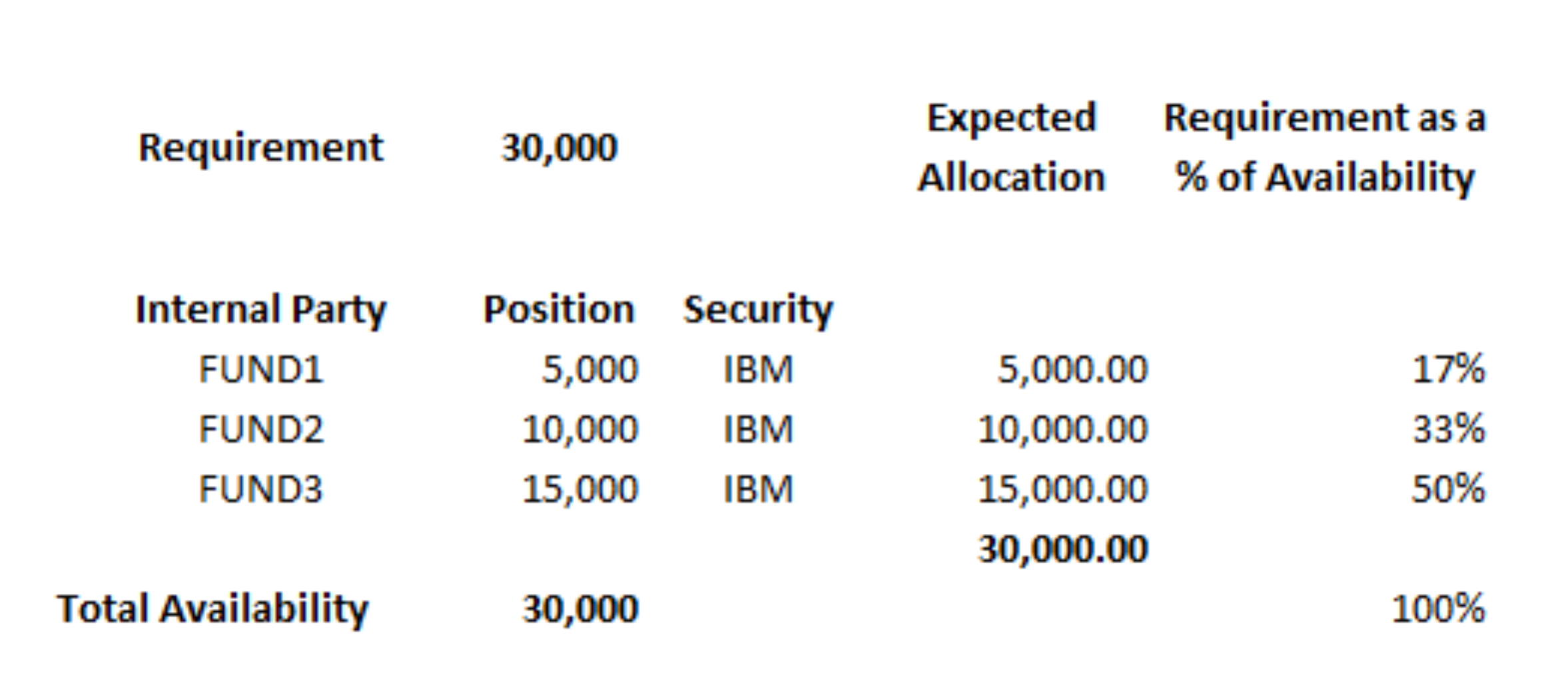

For the size-weighted model, the required quantity allocated to parties with availability is proportional to their availability. So the larger their holding (availability), the larger their contribution to the trade. The downside here is that parties with small holdings will be constantly overlooked by the algorithm as it strives to meet the required quantity in the most efficient manner (i.e. smallest number of shapes).

The required quantity allocated to a client with availability is proportional to their availability, in regards to the size-weighted model.

Figure 3

The algorithmic model and its variants rely on a “league table” of sorts. Versions of this algorithm are regarded as the “fairest” model. To put it simply, this model assigns negative points to “winners” — those parties who got to be selected for a trade — and positive points to “losers” — those parties who were not selected for a trade. Over time, the opportunities even out and every party who has a holding gets to participate in a trade.

The issues

Do we need to worry about Markets in Financial Instruments Directive (MiFID)? Is MiFID applicable to securities lending? The answer is yes. This topic has been debated many times. It seems that the jury is still out with many industry participants believing that it does, and many that it does not.

As a vendor, Broadridge has to cater for both sides of the argument, which in this case means we need to worry about it. By and large, the definition of best execution is mostly applicable to the cash equities market, but what about the other attributes — are they relevant for securities lending? Or what about “Price”? If we take ESMA’s statements literally, no it is probably not. But if you take price to mean rebate or fee rate, then yes. How about “speed of execution of the order and cost”? Speed, not so much. The Securities Financing Transactions Regulation (SFTR) constrains European parties to execute within an hour but, in this context, does it matter if a deal is struck in two, twenty or sixty minutes?

Surely what is more important from a securities lending perspective are the following factors?

Availability — are the securities available for lending and is there sufficient quantity?

Trade type — do I want to do a fee or rebate trade, or perhaps an evergreen?

Rate — am I offered the best fee or rebate rate? It may not be so important for general collateral (GC) business, but it could be essential for specials.

Term — the rate is linked to the term, different rates for open, seven-day and 30 day.

Collateral — triparty or bilateral, and then at a deeper level, what schedule? For example, G10 government bonds or S&P500 equities? Having the right collateral schedule could have a significant impact on the rate you can achieve on a trade.

Relationship — do I have an existing relationship with this party?

Credit or risk-weighted asset — do I have a sufficient credit limit? What is the RWA bucket?

Dividend percentage — what dividend percentage does the borrower need and the lender allow?

If you were going to have a best execution policy for securities lending, wouldn’t the above attributes be the most relevant?

The algorithm

Algorithms really depend on calculating the relative fairness on a fixed set of attributes, but in the real world these attributes may not be at all fixed. There are a lot of ‘what ifs’. For example, what if the borrower only accepts lenders with particular credit ratings? This could rule out whole groups of clients that do not have the requisite credit rating. Additionally, what if the borrower wants a specific term? That is a lot of permutations to build into an algorithm and the associated static data needed to support it — resulting in added complexity. Also, what if the borrowers and lenders have set their default dividend requirements but are flexible? Some lenders would be happy to give up something on the dividend if it was made up elsewhere on the trade.

The challenge with algorithms is that the more complex the algorithms become, the more difficult it is to ascertain what the outcome would be of any allocation. It essentially becomes a “black box” to the trader. It is challenging to build an all-encompassing algorithm that covers every scenario and use case. It is not really desirable or cost effective to try to do so. Where the algorithm fails to provide the best solution, the trader has to step in and override the algorithm.

One could say that as soon as the trader steps in and overrides the allocation, the process is no longer fair, but one could also say that if the trader had to step in then the algorithm failed to find the right match — and if the trader had not stepped in then the trade would have been lost. In this case, a different lender would have been selected as opposed to no lenders selected. What would have been fair about that?

There is no doubt that algorithms will evolve to support the securities lending business as it develops over time. We have to take care that those algorithms remain as fair as is practical, but we also have to be pragmatic as to what is achievable from a technological and human point of view.

A fair algorithmic allocation is the best solution when you have a simple to medium complexity business coupled with high volumes. However, if the business is concentrated on complex trades, then human beings making decisions is an effective and fair alternative.

“Is what fair?”, I hear you ask.

Let’s talk about fair algorithms and just how fair the securities lending business really is. In the agency securities lending world, agents have many fiduciary responsibilities to their underlying clients, be they UCITS funds, family offices or retail clients. These responsibilities encompass many areas outside of the scope of this article, so for the benefit of clarity we will focus on just two of the responsibilities — best execution and fair allocation.

These two concepts are inextricably bound in the business of securities lending, so we cannot talk about one without addressing the other. Before discussing the main topic, it is important to define best execution and fair allocation.

Best execution

“‘Best execution’ means that, when firms execute client orders, they must take all reasonable steps to deliver the best possible result for their clients, taking into account a variety of factors, such as the price of the financial instrument, speed of execution of the order and cost. For retail clients, ‘best possible’ means the most favourable result in terms of the price of the instrument and the costs associated with the execution.”

The above is just one of many definitions of best execution from various European Securities and Markets Authority (ESMA) sources, but there are also legal opinions and a number of different perspectives from members of the International Securities Lending Association (ISLA) and the International Capital Market Association (ICMA).

Fair allocation

With an agency lending trade there are two parties, we have the “street” party, which is the borrower — this could be a prime broker, principal borrower or other sell-side party — and the “internal” party, which is the agent’s internal client — this could be a pension fund, UCITS or any buy-side entity. For example, a generic agency trade.

Figure 1

In the above example, there are three funds lending an aggregate quantity of 30,000 to “STREETCPTY1”.

Borrowers do not want to have piecemeal trades with small quantities, which is why agent lenders aggregate their availability so that they can complete the order in one hit.

The agent lender could have thousands of possible internal clients to select from to fill the trade. The question is — which internal clients should they select for the trade? This is the essence of fair allocation.

There is more than one way to skin the proverbial cat, as is the case with fair allocation. The models that are currently used within the industry can be broken down into variations of several models.

In the equal-allocation model, every internal party gets allocated an equal portion of the trade regardless of the size of parties holding. Although seemingly fair, the downside to this model is the sheer volume of internal allocations that it can generate. It is conceivable to have hundreds, if not thousands, of allocations for a single trade. This can prove expensive for the agent, as each allocation potentially has an associated settlement cost — which can be passed on to the internal client in the form of charges.

A further downside is that the more parties you have on a trade, the more likely it is that firms will have to do a daily reallocation, as the odds are higher, some of the parties that have lent out their shares will have sold them and will need to recall the shares to fulfil the sale. Those parties’ allocation will have to be replaced with shares from another party, otherwise the trade will have to be partially recalled. This issue is not limited to just this allocation model, it applies to any method that creates a large number of allocations.

For the equal-allocation model, the required quantity is equally split among clients with availability.

Figure 2

For the size-weighted model, the required quantity allocated to parties with availability is proportional to their availability. So the larger their holding (availability), the larger their contribution to the trade. The downside here is that parties with small holdings will be constantly overlooked by the algorithm as it strives to meet the required quantity in the most efficient manner (i.e. smallest number of shapes).

The required quantity allocated to a client with availability is proportional to their availability, in regards to the size-weighted model.

Figure 3

The algorithmic model and its variants rely on a “league table” of sorts. Versions of this algorithm are regarded as the “fairest” model. To put it simply, this model assigns negative points to “winners” — those parties who got to be selected for a trade — and positive points to “losers” — those parties who were not selected for a trade. Over time, the opportunities even out and every party who has a holding gets to participate in a trade.

The issues

Do we need to worry about Markets in Financial Instruments Directive (MiFID)? Is MiFID applicable to securities lending? The answer is yes. This topic has been debated many times. It seems that the jury is still out with many industry participants believing that it does, and many that it does not.

As a vendor, Broadridge has to cater for both sides of the argument, which in this case means we need to worry about it. By and large, the definition of best execution is mostly applicable to the cash equities market, but what about the other attributes — are they relevant for securities lending? Or what about “Price”? If we take ESMA’s statements literally, no it is probably not. But if you take price to mean rebate or fee rate, then yes. How about “speed of execution of the order and cost”? Speed, not so much. The Securities Financing Transactions Regulation (SFTR) constrains European parties to execute within an hour but, in this context, does it matter if a deal is struck in two, twenty or sixty minutes?

Surely what is more important from a securities lending perspective are the following factors?

Availability — are the securities available for lending and is there sufficient quantity?

Trade type — do I want to do a fee or rebate trade, or perhaps an evergreen?

Rate — am I offered the best fee or rebate rate? It may not be so important for general collateral (GC) business, but it could be essential for specials.

Term — the rate is linked to the term, different rates for open, seven-day and 30 day.

Collateral — triparty or bilateral, and then at a deeper level, what schedule? For example, G10 government bonds or S&P500 equities? Having the right collateral schedule could have a significant impact on the rate you can achieve on a trade.

Relationship — do I have an existing relationship with this party?

Credit or risk-weighted asset — do I have a sufficient credit limit? What is the RWA bucket?

Dividend percentage — what dividend percentage does the borrower need and the lender allow?

If you were going to have a best execution policy for securities lending, wouldn’t the above attributes be the most relevant?

The algorithm

Algorithms really depend on calculating the relative fairness on a fixed set of attributes, but in the real world these attributes may not be at all fixed. There are a lot of ‘what ifs’. For example, what if the borrower only accepts lenders with particular credit ratings? This could rule out whole groups of clients that do not have the requisite credit rating. Additionally, what if the borrower wants a specific term? That is a lot of permutations to build into an algorithm and the associated static data needed to support it — resulting in added complexity. Also, what if the borrowers and lenders have set their default dividend requirements but are flexible? Some lenders would be happy to give up something on the dividend if it was made up elsewhere on the trade.

The challenge with algorithms is that the more complex the algorithms become, the more difficult it is to ascertain what the outcome would be of any allocation. It essentially becomes a “black box” to the trader. It is challenging to build an all-encompassing algorithm that covers every scenario and use case. It is not really desirable or cost effective to try to do so. Where the algorithm fails to provide the best solution, the trader has to step in and override the algorithm.

One could say that as soon as the trader steps in and overrides the allocation, the process is no longer fair, but one could also say that if the trader had to step in then the algorithm failed to find the right match — and if the trader had not stepped in then the trade would have been lost. In this case, a different lender would have been selected as opposed to no lenders selected. What would have been fair about that?

There is no doubt that algorithms will evolve to support the securities lending business as it develops over time. We have to take care that those algorithms remain as fair as is practical, but we also have to be pragmatic as to what is achievable from a technological and human point of view.

A fair algorithmic allocation is the best solution when you have a simple to medium complexity business coupled with high volumes. However, if the business is concentrated on complex trades, then human beings making decisions is an effective and fair alternative.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times