Native digital assets in securities finance

16 May 2023

In the second of two articles, Dr Ian Hunt notes that, at some point, a major jurisdiction will provide a venue where native digital assets can be issued within a single issuance model and transacted under a single operating model. At that point, securities finance will change profoundly for the better

Image: stock.adobe.com/graphicINmotion

Image: stock.adobe.com/graphicINmotion

Part one of this article - Native digital assets – maximising the benefits of digitisation

Native digital assets offer the prospect of profound benefits to securities financing. These encompass cost reductions for lenders and borrowers, a radical simplification of operational processes, a very high degree of automation and the roll-back of regulation. These benefits are not delivered by doing what we do now, but by applying sexier technology to do things very differently.

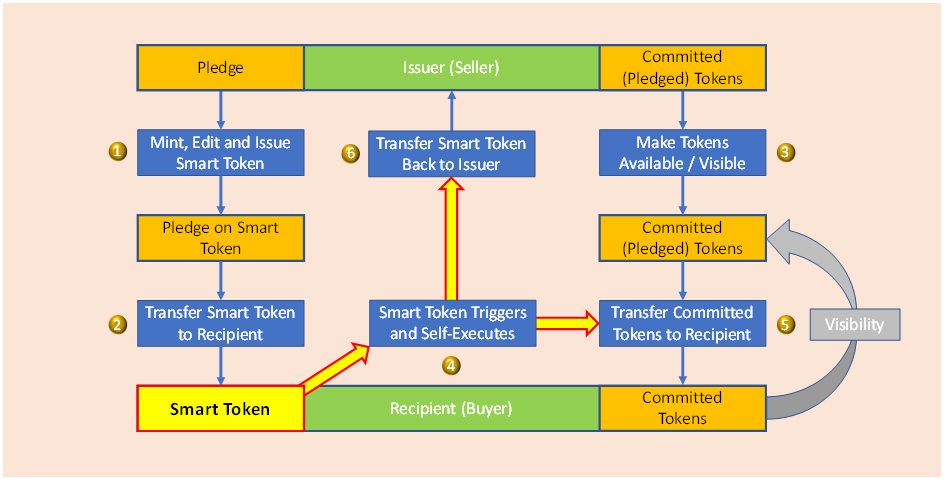

Native digital assets model

In a purely digital financial structure, all transactions are processed in exactly the same way, irrespective of the nature of the transactions or the assets and cash that are being traded. In the digital world, securities finance trades are not unique.

All pots of value are in token form, held at addresses on the ledger. All transactions are flows of tokens between addresses. Native digital assets are just tokens which commit future flows of value and therefore flows of tokens. Smart tokens are just native digital assets which implement and manage the flows that they commit: including flows in securities financing.

The operating model has a tiny number of steps, entities and interactions. There are only five or six steps in the whole process:

• The issuance of the smart token (if the smart token is newly minted, rather than being sold-on by a previous recipient).

• The transfer of the smart token to its recipient.

•The earmarking of the committed tokens by the issuer, making them visible to the recipient.

• The self-initiation of the smart token and the computation of its terms.

• The transfer of the committed tokens from the issuer to the recipient.

• The transfer of the smart token back to the issuer.

Fig 1: Use of smart tokens in securities finance transactions

This process works not just for the settlement of any transaction on the ledger, but also for the other key constituents of our current financial ecosystem: for example, for indications of interest, orders, executions, income payments, corporate actions, collateral transfers and securitisations. It supports not just trading, but also asset servicing, financial engineering and securities finance.

Why securities finance fits the model

The smart token model is based on the self-execution of pledges. The pledges are coded on tokens held on a digital ledger and represent commitments to future flows of value. As outlined above, all value on-ledger is represented in the form of tokens, so those value flows are just flows of tokens between addresses on the same ledger. The pledge tokens are smart, because they have the capability to implement the flows that they commit: they are self-executing, native digital assets. The tokens committed may be cash tokens of some form, may be asset tokens giving title to off-ledger conventional assets or may themselves be native digital assets.

At a superficial level, this set of principles is clearly applicable to securities finance transactions, which are all about commitments to future flows of cash and assets. Those future flows may be the initial movements of cash and collateral in a repo, the exchange of the lent asset for collateral in a stock loan, the periodic adjustment of deposited collateral through valuation and calls, or the return of the lent asset, cash or collateral on termination of a loan or repo.

Why securities finance is different

In most financial transactions, the value exchanged is known and fixed in the trade. In deciding to buy an equity, it would be highly unusual not to have a particular equity specified in the stock leg, and a particular currency specified in the cash leg of the trade. Even in bond trades, where the trading decision may be based on a specification of target terms, conditions and credit quality, a specific bond is identified and baked into the trade order prior to execution. The exact security to be delivered is locked at the point of agreement of the trade, well in advance of settlement.

In securities finance, and generally in collateral agreements, there is a notion of eligibility and substitution. Until the actual delivery of the collateral, the security to be delivered may not be precisely defined. We know its characteristics, defined in an agreement on eligibility, but we do not know its identity. Clearly in stock loans, the lent security itself is known and fixed in the loan agreement. However, the collateral may not be so precise.

In most financial transactions, once the trade is agreed and confirmed contractually, the buyer has a right to the asset and the seller has a right to the cash: the seller can’t pull the sold security back and the buyer can’t claw their cash back.

In securities finance, however, the deliverer of the security sometimes has the right to recall it and to substitute an alternative asset, provided that replacement asset passes the criteria of eligibility. In securities lending, the loaned security can be recalled to enable the lender to benefit from income, corporate actions, voting rights etc. In repo agreements, where there is a termination open specifically agreed between the parties then, again, the deliverer of collateral can recall it at their discretion.

A model based on native digital assets

A typical loan transaction in the smart token model includes three pledges from the lender:

• A commitment to transfer the relevant asset token(s) from the lender to the borrower at the inception of the loan.

• A commitment from the lender to transfer excess collateral tokens back to the borrower on a defined frequency, where the value of the collateral exceeds the value of the lent asset by a defined fraction.

• A commitment from the lender to return the collateral for the lent assets at the termination of the loan or when the lent assets are returned to the lender.

There are four pledges from the borrower:

• A commitment from the borrower to transfer eligible tokens as collateral for the lent assets, at the inception of the loan, in an amount defined as a multiple of the value of the lent assets.

• A commitment from the borrower to transfer the shortfall in collateral tokens to the lender on a defined frequency, when the defined multiple of the value of the lent assets exceeds the value of the collateral.

• A commitment from the borrower to return the asset tokens to the lender at the termination of the loan, or on a defined prior event (such as a recall).

• A commitment from the borrower to pay cash tokens as a fee, in a specified amount and at specified times.

These clusters are exchanged when the loan is agreed, so the lender holds the borrower’s pledges and the borrower holds the lender’s pledges. All of these pledges are issued as smart tokens on the digital ledger and act just like IOUs. There may be other pledges, depending on the nature of the agreed loan. For example, there may be a pledge to deliver cash tokens representing manufactured dividends from the borrower to the lender. In any case, the pledges are all just smart tokens like any other and will self-activate and will implement their own terms.

In a fully digital system of finance, ownership is a simple construct: it is the location of a token. If the token is held at your address on the digital ledger, then you own the token. Any lien, mortgage, claim, charge or encumbrance on the token is represented simply by a pledge to deliver it in future, and under defined conditions, to the holder of the charge. As a result, a repo is very similar to a loan in the smart token model.

However, there are some differences between a native digital loan and a native digital repo. The fee pledge in the loan does not exist for the repo and the primary tokens transferred in the repo are always cash tokens. The collateral in a loan is often, but not always, cash tokens while the collateral in a repo is generally a set of asset tokens; these may be tokenised conventional assets or may be native digital assets. On termination of the repo, the asset tokens are returned, but the cash tokens returned are inflated by the repo rate agreed for the transaction and the time over which the cash tokens have been held. The termination date of the repo is generally fixed and short-term, but undefined if it is an open repo. For stock loans, the tenor is generally unlimited and termination is on recall or return of the loaned stock.

Handling the differences in securities finance

The differences outlined above for securities finance and collateral management require some extension of the native digital assets model. In the simplest form of the model, each smart token implements the transfer of tokens whose identity is pre-defined. The availability for transfer of those committed tokens is exposed across the ledger: the recipient has visibility of the committed tokens on the issuer’s node. The recipient can confirm both the identity and the quantum of the tokens earmarked for delivery and this can enhance trust as a result.

In a securities finance context, the identity of the tokens to be delivered may not be known until they are earmarked for delivery. The smart token that manages their delivery therefore needs to carry the eligibility criteria, rather than the identity of the tokens to be transferred. When the committed tokens are made visible to the recipient, then the smart token (on behalf of the recipient) needs to check that the tokens satisfy the eligibility criteria.

To accommodate recalls, substitutions and upgrades, additional pledges are required from both the issuer/lender and the recipient/borrower. The issuer needs to pledge the return of the collateral on request from the recipient and the recipient needs to pledge the delivery of replacement eligible collateral on receipt of the recalled collateral.

The benefits of a native digital model

The parties to a securities finance transaction deploying native digital assets will benefit from a very high degree of automation. Once issued by an issuer and held by a recipient, the smart tokens do all the work: they calculate, validate, trigger and manage the movements of assets and cash which implement the transaction throughout its lifecycle. The tokens do this within a very simple operating model that is shared across asset types and products. With a single, simple operating model, the complexity of technology reduces markedly, even though the level of automation goes up.

Because there is a single operating model, the sharing of infrastructure and people across a financial organisation becomes wholly practical. Securities finance is no longer an island of custom process and technology. Neither are funds, derivatives, income or corporate actions: all of these apparently disparate assets, activities and products are managed in exactly the same way, under the same operating model and deploying the same platform.

To implement a new contract type, accommodate a new asset class, create new terms or new eligibility criteria, all that the parties need to do is to issue and code the appropriate smart tokens. No infrastructural, technical, operating model or security data changes are necessary. As a consequence, change is very quick and very cheap.

The fact that there is only one digital operating model, and the tiny number of entities, objects and processes that it deploys, reduces the required regulation by multiple orders of magnitude. As a result of the very high level of automation, the reduction in the number of intermediary entities and the simplification of regulation, costs to both lenders and borrowers are reduced substantially.

At some point, a major jurisdiction will provide a venue where native digital assets can be issued within a single issuance model and transacted under a single operating model. At that point, securities finance will change profoundly, permanently and much for the better. Other jurisdictions will have no choice but to follow suit.

Native digital assets offer the prospect of profound benefits to securities financing. These encompass cost reductions for lenders and borrowers, a radical simplification of operational processes, a very high degree of automation and the roll-back of regulation. These benefits are not delivered by doing what we do now, but by applying sexier technology to do things very differently.

Native digital assets model

In a purely digital financial structure, all transactions are processed in exactly the same way, irrespective of the nature of the transactions or the assets and cash that are being traded. In the digital world, securities finance trades are not unique.

All pots of value are in token form, held at addresses on the ledger. All transactions are flows of tokens between addresses. Native digital assets are just tokens which commit future flows of value and therefore flows of tokens. Smart tokens are just native digital assets which implement and manage the flows that they commit: including flows in securities financing.

The operating model has a tiny number of steps, entities and interactions. There are only five or six steps in the whole process:

• The issuance of the smart token (if the smart token is newly minted, rather than being sold-on by a previous recipient).

• The transfer of the smart token to its recipient.

•The earmarking of the committed tokens by the issuer, making them visible to the recipient.

• The self-initiation of the smart token and the computation of its terms.

• The transfer of the committed tokens from the issuer to the recipient.

• The transfer of the smart token back to the issuer.

Fig 1: Use of smart tokens in securities finance transactions

This process works not just for the settlement of any transaction on the ledger, but also for the other key constituents of our current financial ecosystem: for example, for indications of interest, orders, executions, income payments, corporate actions, collateral transfers and securitisations. It supports not just trading, but also asset servicing, financial engineering and securities finance.

Why securities finance fits the model

The smart token model is based on the self-execution of pledges. The pledges are coded on tokens held on a digital ledger and represent commitments to future flows of value. As outlined above, all value on-ledger is represented in the form of tokens, so those value flows are just flows of tokens between addresses on the same ledger. The pledge tokens are smart, because they have the capability to implement the flows that they commit: they are self-executing, native digital assets. The tokens committed may be cash tokens of some form, may be asset tokens giving title to off-ledger conventional assets or may themselves be native digital assets.

At a superficial level, this set of principles is clearly applicable to securities finance transactions, which are all about commitments to future flows of cash and assets. Those future flows may be the initial movements of cash and collateral in a repo, the exchange of the lent asset for collateral in a stock loan, the periodic adjustment of deposited collateral through valuation and calls, or the return of the lent asset, cash or collateral on termination of a loan or repo.

Why securities finance is different

In most financial transactions, the value exchanged is known and fixed in the trade. In deciding to buy an equity, it would be highly unusual not to have a particular equity specified in the stock leg, and a particular currency specified in the cash leg of the trade. Even in bond trades, where the trading decision may be based on a specification of target terms, conditions and credit quality, a specific bond is identified and baked into the trade order prior to execution. The exact security to be delivered is locked at the point of agreement of the trade, well in advance of settlement.

In securities finance, and generally in collateral agreements, there is a notion of eligibility and substitution. Until the actual delivery of the collateral, the security to be delivered may not be precisely defined. We know its characteristics, defined in an agreement on eligibility, but we do not know its identity. Clearly in stock loans, the lent security itself is known and fixed in the loan agreement. However, the collateral may not be so precise.

In most financial transactions, once the trade is agreed and confirmed contractually, the buyer has a right to the asset and the seller has a right to the cash: the seller can’t pull the sold security back and the buyer can’t claw their cash back.

In securities finance, however, the deliverer of the security sometimes has the right to recall it and to substitute an alternative asset, provided that replacement asset passes the criteria of eligibility. In securities lending, the loaned security can be recalled to enable the lender to benefit from income, corporate actions, voting rights etc. In repo agreements, where there is a termination open specifically agreed between the parties then, again, the deliverer of collateral can recall it at their discretion.

A model based on native digital assets

A typical loan transaction in the smart token model includes three pledges from the lender:

• A commitment to transfer the relevant asset token(s) from the lender to the borrower at the inception of the loan.

• A commitment from the lender to transfer excess collateral tokens back to the borrower on a defined frequency, where the value of the collateral exceeds the value of the lent asset by a defined fraction.

• A commitment from the lender to return the collateral for the lent assets at the termination of the loan or when the lent assets are returned to the lender.

There are four pledges from the borrower:

• A commitment from the borrower to transfer eligible tokens as collateral for the lent assets, at the inception of the loan, in an amount defined as a multiple of the value of the lent assets.

• A commitment from the borrower to transfer the shortfall in collateral tokens to the lender on a defined frequency, when the defined multiple of the value of the lent assets exceeds the value of the collateral.

• A commitment from the borrower to return the asset tokens to the lender at the termination of the loan, or on a defined prior event (such as a recall).

• A commitment from the borrower to pay cash tokens as a fee, in a specified amount and at specified times.

These clusters are exchanged when the loan is agreed, so the lender holds the borrower’s pledges and the borrower holds the lender’s pledges. All of these pledges are issued as smart tokens on the digital ledger and act just like IOUs. There may be other pledges, depending on the nature of the agreed loan. For example, there may be a pledge to deliver cash tokens representing manufactured dividends from the borrower to the lender. In any case, the pledges are all just smart tokens like any other and will self-activate and will implement their own terms.

In a fully digital system of finance, ownership is a simple construct: it is the location of a token. If the token is held at your address on the digital ledger, then you own the token. Any lien, mortgage, claim, charge or encumbrance on the token is represented simply by a pledge to deliver it in future, and under defined conditions, to the holder of the charge. As a result, a repo is very similar to a loan in the smart token model.

However, there are some differences between a native digital loan and a native digital repo. The fee pledge in the loan does not exist for the repo and the primary tokens transferred in the repo are always cash tokens. The collateral in a loan is often, but not always, cash tokens while the collateral in a repo is generally a set of asset tokens; these may be tokenised conventional assets or may be native digital assets. On termination of the repo, the asset tokens are returned, but the cash tokens returned are inflated by the repo rate agreed for the transaction and the time over which the cash tokens have been held. The termination date of the repo is generally fixed and short-term, but undefined if it is an open repo. For stock loans, the tenor is generally unlimited and termination is on recall or return of the loaned stock.

Handling the differences in securities finance

The differences outlined above for securities finance and collateral management require some extension of the native digital assets model. In the simplest form of the model, each smart token implements the transfer of tokens whose identity is pre-defined. The availability for transfer of those committed tokens is exposed across the ledger: the recipient has visibility of the committed tokens on the issuer’s node. The recipient can confirm both the identity and the quantum of the tokens earmarked for delivery and this can enhance trust as a result.

In a securities finance context, the identity of the tokens to be delivered may not be known until they are earmarked for delivery. The smart token that manages their delivery therefore needs to carry the eligibility criteria, rather than the identity of the tokens to be transferred. When the committed tokens are made visible to the recipient, then the smart token (on behalf of the recipient) needs to check that the tokens satisfy the eligibility criteria.

To accommodate recalls, substitutions and upgrades, additional pledges are required from both the issuer/lender and the recipient/borrower. The issuer needs to pledge the return of the collateral on request from the recipient and the recipient needs to pledge the delivery of replacement eligible collateral on receipt of the recalled collateral.

The benefits of a native digital model

The parties to a securities finance transaction deploying native digital assets will benefit from a very high degree of automation. Once issued by an issuer and held by a recipient, the smart tokens do all the work: they calculate, validate, trigger and manage the movements of assets and cash which implement the transaction throughout its lifecycle. The tokens do this within a very simple operating model that is shared across asset types and products. With a single, simple operating model, the complexity of technology reduces markedly, even though the level of automation goes up.

Because there is a single operating model, the sharing of infrastructure and people across a financial organisation becomes wholly practical. Securities finance is no longer an island of custom process and technology. Neither are funds, derivatives, income or corporate actions: all of these apparently disparate assets, activities and products are managed in exactly the same way, under the same operating model and deploying the same platform.

To implement a new contract type, accommodate a new asset class, create new terms or new eligibility criteria, all that the parties need to do is to issue and code the appropriate smart tokens. No infrastructural, technical, operating model or security data changes are necessary. As a consequence, change is very quick and very cheap.

The fact that there is only one digital operating model, and the tiny number of entities, objects and processes that it deploys, reduces the required regulation by multiple orders of magnitude. As a result of the very high level of automation, the reduction in the number of intermediary entities and the simplification of regulation, costs to both lenders and borrowers are reduced substantially.

At some point, a major jurisdiction will provide a venue where native digital assets can be issued within a single issuance model and transacted under a single operating model. At that point, securities finance will change profoundly, permanently and much for the better. Other jurisdictions will have no choice but to follow suit.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times