US repo comes into the regulatory spotlight

01 October 2024

With new rules and guidelines coming from the SEC and the OFR, Ed Tyndale-Biscoe, head of secured funding product development at ION, looks at the importance of the US repo market as a linchpin in the financial system

Image: Shutterstock

Image: Shutterstock

Volatility is unsettling. Especially when it cannot be explained or was not predicted. Regulators react by tightening procedures, market participants adapt to the new realities, and platforms emerge to seize opportunities. In times of upheaval, getting the most out of the latest advances in technology can become a question of business survival.

Nowhere is this more relevant than in repo, where trillions of dollars flow daily to cater to the funding needs of financial institutions, and governments signal monetary policy. But there is a problem — a large chunk is out of regulatory sight. That is about to change.

Earlier this summer, the Office of Financial Research (OFR), a research entity under the US Treasury Department, finalised a rule to collect data on non-centrally cleared bilateral repurchase agreements (NCCBR).

The repo market allows banks and other firms to borrow cash for short periods using collateral like high-quality government securities and this new legislation aims to shed light on NCCBR transactions, which have remained largely opaque despite being the largest segment of the repo market. Recent data shows daily outstanding commitments exceeding US$2 trillion.

Attributes of US repo markets

This product type is popular with investors, especially hedge funds, due to the flexibility in contract terms such as haircuts and margin, which are crucial in determining transaction pricing, as they dictate the leverage on individual trades.

The OFR states that “permanent data collection will shine a spotlight into this opaque corner of the financial market, provide high-quality data on NCCBR transactions, and remove a significant blind spot for financial regulators”.

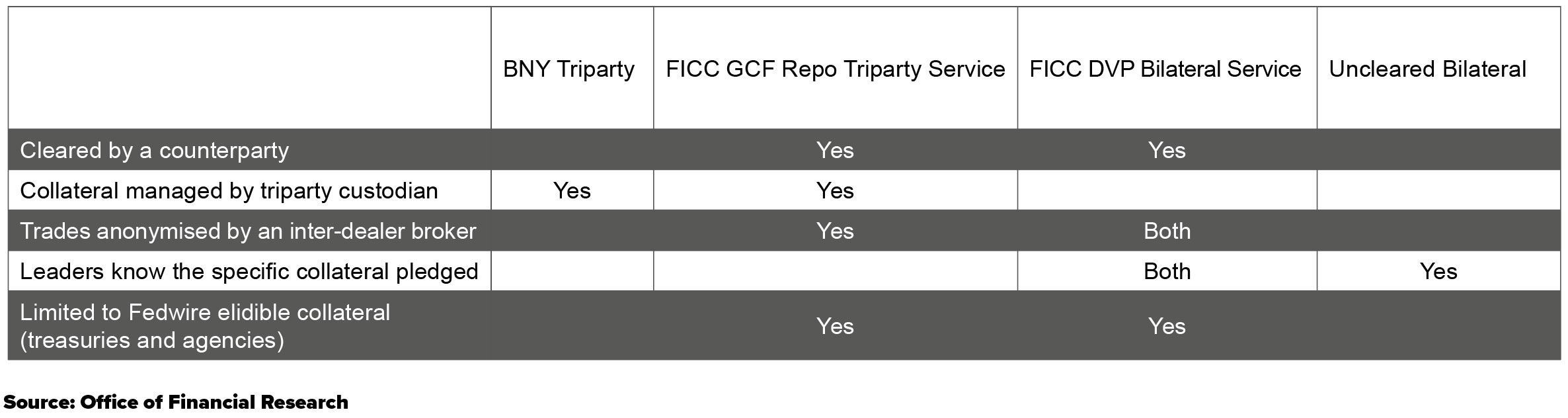

In contrast, centrally cleared and triparty repo sections are already regulated in the US and Europe. The OFR began data collection for the US market five years ago, while firms offering triparty services follow national and regional rules. This involves an independent institution, like a clearing bank or central securities depository (CSD), acting as an intermediary to manage the administration between the two parties in the repo transaction.

Different compliance deadlines

The OFR’s data collection requirement, effective from 5 July 2024, covers 32 data fields and applies to two categories of firms with different compliance deadlines. The first group, comprising around 40 firms, including brokers and dealers, has until 2 December 2024 to comply. These firms have significant daily commitments in NCCBR transactions. The second, smaller group, which includes other financial companies, has until 1 April 2025, followed by an additional three months to fully comply.

The groundwork for this regulation began in 2022, but the OFR only submitted a concrete proposal in early 2023 after the Financial Stability Oversight Council’s urging. A consultation was launched in March 2023, and the final rule was published in May 2024.

The lack of transparency in the repo market became a critical issue in September 2019 when increased government borrowing led to a shortage of bank reserves, causing repo interest rates to spike from 2.43 per cent to 5.25 per cent, and at one point exceeding 10 per cent. The Federal Reserve had to inject approximately US$350 billion into the market to stabilise it.

The market was relatively stable until December 2023, when quantitative tightening to curb inflation caused significant fluctuations in short-term loan markets. The Depository Trust & Clearing Corporation (DTCC) GCF Treasury Repo Index, which tracks the average daily interest rate for the most traded general collateral finance repo contracts for US Treasuries, jumped from 5.395 per cent to 5.45 per cent in the last week of December 2023.

Push for transparency and clearing

Although December 2023’s volatility was less severe than in 2019, and the furore soon died down, it again highlighted the repo market’s importance in the smooth operation of the global financial system and the need for transparency to understand market movements.

New US Securities and Exchange Commission (SEC) rules, effective in phases by June 2026, will require cash and repo transactions in US Treasury securities (UST) to be centrally cleared. “The USD 26 trillion Treasury market — the deepest, most liquid market in the world — is the base upon which so much of our capital markets are built,” said SEC Chair Gary Gensler last year. “Having such a significant portion of the Treasury markets uncleared — 70 to 80 per cent of the Treasury funding market and at least 80 per cent of the cash markets — increases system-wide risk.’’

While regulators need comprehensive market data to assess systemic risk, market participants must prepare for more rigorous daily transaction reporting. It is safe to say that some uncertainty exists about the impact these changes will have, never mind the readiness of the market to move to this model, given that it is now less than 18 months until the first phase comes into effect. While there may be a general consensus that the changes will improve market resilience and reduce contagion risk (the knock-on impact of a market specific scenario spreading) there seems to be widespread uncertainty about the cost and market liquidity consequences in the short and medium term.

ION recently detailed the scope of the mandate, Fixed Income Clearing Corporation (FICC) access methods, and financial costs associated with UST repos clearing after the SEC mandate goes live in mid-2026. But what will remain of uncleared UST repo activity after that date?

The SEC’s UST clearing mandate requires any UST central counterparty clearing house (CCP) to amend its rulebook, mandating direct participants (ie bank ‘netting members’) to clear all UST trades with in-scope counterparties. However, uncleared UST trades will still be allowed in two scenarios:

1. Between a direct participant and an out-of-scope counterparty.

2. Between two non-direct participants.

Another aspect to consider is done-away clearing, the practice of trading with one dealer and clearing the trade with another. A recent Greenwich Coalition report said it is expected “to be the norm when the dust settles, but the path toward the final model is going to take time”. For done-away to thrive, as it does in derivatives, it may require comprehensive market-wide automation across clients, dealers, and FICC.

Interbank and central bank trades

Even before the mandate, UST repos between two FICC netting member banks were regularly cleared for regulatory capital advantages, such as reducing leverage ratios and risk-weighted assets (RWA). US banks must clear their UST trades with US dealers. Non-US banks, being out of scope, can continue trading uncleared UST repo. However, the capital burden from local Basel III implementations may incentivise them to clear via sponsored or agent clearing or by becoming netting members.

Since the 2008 global financial crisis, the Fed has been more involved in the repo markets through new secured funding facilities. These facilities are here to stay as they complement traditional quantitative easing (QE) tools and provide short-term cash injections for managing severe end-of-day cash liquidity shortages or surpluses.

Banks, foreign central banks, and authorised money funds and hedge funds can use these facilities to park or raise cash from the Fed in exchange for US government bonds, including USTs. The Fed and other central banks are out-of-scope counterparties for the mandate, so their trades are not required to clear.

Buy side trades

Beyond banks and central banks, UST repo buy side clients include non-bank financial firms that want to borrow or lend cash against UST. These are usually hedge funds (borrowing cash to create leverage) and money market funds (lending cash for a safe return). Other buy side investors, like traditional asset managers or insurance companies, typically invest cash one-time or unleveraged in buy-and-hold securities and do not lend or borrow cash.

Currently, money funds and hedge funds always trade repo with a dealer, because money fund credit policies prohibit direct exposure to leveraged, lower credit-rated hedge funds. A dealer bank stands in between as principal, generating two dealer-to-client (D2C) repos. D2C UST repos with US financial firms will be required to clear after mid-2026, impacting banks financially. Foreign buy side firms will be exempt, but banks may charge higher spreads or increase haircuts on uncleared trades, discouraging such activity.

The impact that clearing will have on this segment of the repo market is interesting — sell side firms, acting as the bridge between the less tightly regulated parties already have to manage higher capital costs. Central clearing may increase these, reducing the spreads they can achieve and hence impacting liquidity. The buy sides, however, may be betting on a more commoditised, and competitive market, and tighter spreads.

New repo markets

Post-mandate, uncleared UST repo activity will primarily involve trades with central bank facilities and a small volume with foreign banks and buy side firms. Some vendors are innovating to change this with new firms introducing peer-to-peer trading platforms, where clients trade directly via a proprietary protocol, with a sole broker-guarantor, or via new multi-dealer trading platforms, where dealers compete to broker and guarantee client-to-client repos based on standardised trading and guarantee documents.

Guaranteed repos on these platforms work as follows:

• The repo executes and settles directly between two client principals with operational assistance from the platform.

• A bank brokers the repo but is not a principal, so clearing is not required.

• The bank guarantees the money fund, stepping in if the hedge fund defaults.

Money funds can only engage in such trades if they are comfortable with the credit exposure transfer from the hedge fund to the bank. Providers claim banks receive favourable capital treatment over both cleared and D2C uncleared repos.

What can we conclude?

In summary, banks will still broker trades and provide hedge fund credit upgrades via guarantees instead of intermediating as principals. After the SEC clearing mandate goes live in mid-2026, uncleared UST repos will include Fed facilities trades and limited foreign bank and financial firm trades. The extent of guaranteed repo activity will depend on participants’ willingness to invest in the necessary infrastructure.

The path to the clearing mandate going live is a phased one but market participants should be ready to act quickly. Just like the move to a shorter settlement period (T+1), firms should be preparing and testing for all scenarios long before 2026. Any mistakes in this corner of the market, the lifeblood of the system — where financial institutions can meet their day-to-day funding needs and governments transmit monetary policy through interest rates — will have costly implications beyond the immediate affected markets.

Some consideration should be given to whether the market, post-implementation, will morph into an extension of the futures market, where standardisation simplifies access for a broader range of participants, even if the overall costs for everyone involved increase to cope with the additional margin, clearing and capital costs. Futures and repo markets are very different for a wide variety of reasons, but lessons from the swap clearing mandates over the last decade can be learned.

In times of evolving regulations, cost pressures, market and political uncertainty, firms should look at their workflows and processes. Those relying on disjointed and outdated technology must act now and future-proof their business. In what is largely a scale business model, simplifying and automating trading and risk management workflows, increasing trading via electronic platforms, consolidating and executing tasks in one system, and having a holistic view of business in real time are the optimal route to achieving this.

Nowhere is this more relevant than in repo, where trillions of dollars flow daily to cater to the funding needs of financial institutions, and governments signal monetary policy. But there is a problem — a large chunk is out of regulatory sight. That is about to change.

Earlier this summer, the Office of Financial Research (OFR), a research entity under the US Treasury Department, finalised a rule to collect data on non-centrally cleared bilateral repurchase agreements (NCCBR).

The repo market allows banks and other firms to borrow cash for short periods using collateral like high-quality government securities and this new legislation aims to shed light on NCCBR transactions, which have remained largely opaque despite being the largest segment of the repo market. Recent data shows daily outstanding commitments exceeding US$2 trillion.

Attributes of US repo markets

This product type is popular with investors, especially hedge funds, due to the flexibility in contract terms such as haircuts and margin, which are crucial in determining transaction pricing, as they dictate the leverage on individual trades.

The OFR states that “permanent data collection will shine a spotlight into this opaque corner of the financial market, provide high-quality data on NCCBR transactions, and remove a significant blind spot for financial regulators”.

In contrast, centrally cleared and triparty repo sections are already regulated in the US and Europe. The OFR began data collection for the US market five years ago, while firms offering triparty services follow national and regional rules. This involves an independent institution, like a clearing bank or central securities depository (CSD), acting as an intermediary to manage the administration between the two parties in the repo transaction.

Different compliance deadlines

The OFR’s data collection requirement, effective from 5 July 2024, covers 32 data fields and applies to two categories of firms with different compliance deadlines. The first group, comprising around 40 firms, including brokers and dealers, has until 2 December 2024 to comply. These firms have significant daily commitments in NCCBR transactions. The second, smaller group, which includes other financial companies, has until 1 April 2025, followed by an additional three months to fully comply.

The groundwork for this regulation began in 2022, but the OFR only submitted a concrete proposal in early 2023 after the Financial Stability Oversight Council’s urging. A consultation was launched in March 2023, and the final rule was published in May 2024.

The lack of transparency in the repo market became a critical issue in September 2019 when increased government borrowing led to a shortage of bank reserves, causing repo interest rates to spike from 2.43 per cent to 5.25 per cent, and at one point exceeding 10 per cent. The Federal Reserve had to inject approximately US$350 billion into the market to stabilise it.

The market was relatively stable until December 2023, when quantitative tightening to curb inflation caused significant fluctuations in short-term loan markets. The Depository Trust & Clearing Corporation (DTCC) GCF Treasury Repo Index, which tracks the average daily interest rate for the most traded general collateral finance repo contracts for US Treasuries, jumped from 5.395 per cent to 5.45 per cent in the last week of December 2023.

Push for transparency and clearing

Although December 2023’s volatility was less severe than in 2019, and the furore soon died down, it again highlighted the repo market’s importance in the smooth operation of the global financial system and the need for transparency to understand market movements.

New US Securities and Exchange Commission (SEC) rules, effective in phases by June 2026, will require cash and repo transactions in US Treasury securities (UST) to be centrally cleared. “The USD 26 trillion Treasury market — the deepest, most liquid market in the world — is the base upon which so much of our capital markets are built,” said SEC Chair Gary Gensler last year. “Having such a significant portion of the Treasury markets uncleared — 70 to 80 per cent of the Treasury funding market and at least 80 per cent of the cash markets — increases system-wide risk.’’

While regulators need comprehensive market data to assess systemic risk, market participants must prepare for more rigorous daily transaction reporting. It is safe to say that some uncertainty exists about the impact these changes will have, never mind the readiness of the market to move to this model, given that it is now less than 18 months until the first phase comes into effect. While there may be a general consensus that the changes will improve market resilience and reduce contagion risk (the knock-on impact of a market specific scenario spreading) there seems to be widespread uncertainty about the cost and market liquidity consequences in the short and medium term.

ION recently detailed the scope of the mandate, Fixed Income Clearing Corporation (FICC) access methods, and financial costs associated with UST repos clearing after the SEC mandate goes live in mid-2026. But what will remain of uncleared UST repo activity after that date?

The SEC’s UST clearing mandate requires any UST central counterparty clearing house (CCP) to amend its rulebook, mandating direct participants (ie bank ‘netting members’) to clear all UST trades with in-scope counterparties. However, uncleared UST trades will still be allowed in two scenarios:

1. Between a direct participant and an out-of-scope counterparty.

2. Between two non-direct participants.

Another aspect to consider is done-away clearing, the practice of trading with one dealer and clearing the trade with another. A recent Greenwich Coalition report said it is expected “to be the norm when the dust settles, but the path toward the final model is going to take time”. For done-away to thrive, as it does in derivatives, it may require comprehensive market-wide automation across clients, dealers, and FICC.

Interbank and central bank trades

Even before the mandate, UST repos between two FICC netting member banks were regularly cleared for regulatory capital advantages, such as reducing leverage ratios and risk-weighted assets (RWA). US banks must clear their UST trades with US dealers. Non-US banks, being out of scope, can continue trading uncleared UST repo. However, the capital burden from local Basel III implementations may incentivise them to clear via sponsored or agent clearing or by becoming netting members.

Since the 2008 global financial crisis, the Fed has been more involved in the repo markets through new secured funding facilities. These facilities are here to stay as they complement traditional quantitative easing (QE) tools and provide short-term cash injections for managing severe end-of-day cash liquidity shortages or surpluses.

Banks, foreign central banks, and authorised money funds and hedge funds can use these facilities to park or raise cash from the Fed in exchange for US government bonds, including USTs. The Fed and other central banks are out-of-scope counterparties for the mandate, so their trades are not required to clear.

Buy side trades

Beyond banks and central banks, UST repo buy side clients include non-bank financial firms that want to borrow or lend cash against UST. These are usually hedge funds (borrowing cash to create leverage) and money market funds (lending cash for a safe return). Other buy side investors, like traditional asset managers or insurance companies, typically invest cash one-time or unleveraged in buy-and-hold securities and do not lend or borrow cash.

Currently, money funds and hedge funds always trade repo with a dealer, because money fund credit policies prohibit direct exposure to leveraged, lower credit-rated hedge funds. A dealer bank stands in between as principal, generating two dealer-to-client (D2C) repos. D2C UST repos with US financial firms will be required to clear after mid-2026, impacting banks financially. Foreign buy side firms will be exempt, but banks may charge higher spreads or increase haircuts on uncleared trades, discouraging such activity.

The impact that clearing will have on this segment of the repo market is interesting — sell side firms, acting as the bridge between the less tightly regulated parties already have to manage higher capital costs. Central clearing may increase these, reducing the spreads they can achieve and hence impacting liquidity. The buy sides, however, may be betting on a more commoditised, and competitive market, and tighter spreads.

New repo markets

Post-mandate, uncleared UST repo activity will primarily involve trades with central bank facilities and a small volume with foreign banks and buy side firms. Some vendors are innovating to change this with new firms introducing peer-to-peer trading platforms, where clients trade directly via a proprietary protocol, with a sole broker-guarantor, or via new multi-dealer trading platforms, where dealers compete to broker and guarantee client-to-client repos based on standardised trading and guarantee documents.

Guaranteed repos on these platforms work as follows:

• The repo executes and settles directly between two client principals with operational assistance from the platform.

• A bank brokers the repo but is not a principal, so clearing is not required.

• The bank guarantees the money fund, stepping in if the hedge fund defaults.

Money funds can only engage in such trades if they are comfortable with the credit exposure transfer from the hedge fund to the bank. Providers claim banks receive favourable capital treatment over both cleared and D2C uncleared repos.

What can we conclude?

In summary, banks will still broker trades and provide hedge fund credit upgrades via guarantees instead of intermediating as principals. After the SEC clearing mandate goes live in mid-2026, uncleared UST repos will include Fed facilities trades and limited foreign bank and financial firm trades. The extent of guaranteed repo activity will depend on participants’ willingness to invest in the necessary infrastructure.

The path to the clearing mandate going live is a phased one but market participants should be ready to act quickly. Just like the move to a shorter settlement period (T+1), firms should be preparing and testing for all scenarios long before 2026. Any mistakes in this corner of the market, the lifeblood of the system — where financial institutions can meet their day-to-day funding needs and governments transmit monetary policy through interest rates — will have costly implications beyond the immediate affected markets.

Some consideration should be given to whether the market, post-implementation, will morph into an extension of the futures market, where standardisation simplifies access for a broader range of participants, even if the overall costs for everyone involved increase to cope with the additional margin, clearing and capital costs. Futures and repo markets are very different for a wide variety of reasons, but lessons from the swap clearing mandates over the last decade can be learned.

In times of evolving regulations, cost pressures, market and political uncertainty, firms should look at their workflows and processes. Those relying on disjointed and outdated technology must act now and future-proof their business. In what is largely a scale business model, simplifying and automating trading and risk management workflows, increasing trading via electronic platforms, consolidating and executing tasks in one system, and having a holistic view of business in real time are the optimal route to achieving this.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times